Growing a business requires more than a great idea; it requires access to the right financing at the right time. Whether you’re expanding your operations, purchasing equipment, hiring employees, or managing cash flow, business term loans provide one of the most dependable funding solutions available for small and medium-sized businesses.

Unlike revolving credit, a term loan gives your business a lump sum of capital upfront, which is repaid over a fixed period through scheduled monthly payments. This predictable repayment structure makes budgeting easier while helping businesses invest confidently in long-term growth.

Key Takeaways

- Business term loans provide a lump sum of capital with fixed repayment terms.

- They are commonly used for expansion, equipment purchases, inventory, working capital, and refinancing.

- Loan options include short-, intermediate-, and long-term financing, as well as secured and unsecured loans.

- Fixed-rate loans offer predictable payments, while variable-rate loans may fluctuate over time.

- Strong revenue, healthy credit, and organized financial records can improve approval chances.

- Comparing lenders and understanding the total cost of borrowing helps businesses choose the right financing solution.

At Committed to Capital, we help business owners secure financing that matches their goals not just the fastest approval. Our team works with trusted lending partners to simplify the borrowing process, reduce unnecessary paperwork, and connect businesses with competitive financing solutions tailored to their needs.

Whether you’re launching a new expansion strategy or strengthening working capital, understanding how business term loans work can help you make smarter financial decisions.

What is a Business Term Loan?

A business term loan is a financing solution where a lender provides your business with a fixed amount of money upfront. In return, you repay the loan over an agreed period through regular installments that include both principal and interest.

Unlike a business line of credit, which allows you to borrow repeatedly as needed, a term loan provides a one-time funding amount designed for specific business investments.

Businesses commonly use term loans to finance equipment purchases, expansion projects, office renovations, inventory, hiring, working capital, marketing campaigns, commercial property, and refinancing existing debt.

Because repayment terms are clearly defined from the beginning, business owners know exactly how much they will pay each month, making long-term financial planning easier.

How Business Term Loans Work

Business term loans follow a straightforward application and funding process. While requirements may vary by lender, the typical process includes the following steps:

1. Submit Your Loan Application

Provide basic information about your business, including:

- Business name and industry

- Time in business

- Annual or monthly revenue

- Recent business bank statements

- Tax returns (if required)

- Personal and business credit information

This information helps lenders understand your company’s financial health and eligibility.

2. Lender Reviews Your Application

After receiving your application, the lender evaluates several key factors, including:

- Revenue consistency

- Cash flow

- Existing debt obligations

- Business and personal credit history

- Overall business performance

- Ability to repay the loan

Some lenders may also consider your industry, years in operation, and future growth potential during the underwriting process.

3. Receive a Loan Offer

If your application is approved, the lender provides a loan offer outlining:

- Loan amount

- Interest rate

- Repayment term

- Monthly payment amount

- Applicable fees

- Funding conditions

Review these terms carefully to ensure the financing aligns with your business goals and budget.

4. Accept the Loan Agreement

Once you’re satisfied with the loan terms, you’ll sign the financing agreement and complete any remaining verification requirements before funding.

5. Receive Your Funds

After the agreement is finalized, the lender deposits the approved loan amount directly into your business bank account.

Funding timelines vary by lender, but many online lenders provide funding within 24 to 72 hours. Businesses with urgent financing needs may also consider same-day business loans when available.

6. Repay the Loan

Repayment begins according to the agreed schedule, typically through fixed monthly installments that include both principal and interest.

Making on-time payments helps build your business credit profile and can improve your eligibility for future financing opportunities.

Types of Business Term Loans

Business financing is not one-size-fits-all. Different loan structures serve different business goals.

Short-Term Business Loans

Short-term loans generally have repayment periods of 3 to 12 months. They are commonly used for seasonal inventory, payroll expenses, emergency repairs, marketing campaigns, and temporary cash flow shortages.

Although they provide quick access to capital, they often carry higher monthly payments because of the shorter repayment period.

Intermediate-Term Business Loans

Intermediate-term loans typically range from one to five years. These loans are well suited for businesses planning moderate investments, including equipment upgrades, technology improvements, vehicle purchases, office remodeling, and expanding product lines.

Long-Term Business Loans

Long-term loans generally extend from five to ten years or more, depending on the lender and loan purpose.

Businesses often use long-term financing for commercial real estate, major renovations, acquisitions, franchise expansion, large equipment purchases, and manufacturing facilities. Business owners considering property-related financing may also benefit from reviewing commercial mortgage loan tips.

Secured Business Term Loans

Secured loans require collateral such as equipment, commercial property, vehicles, inventory, or accounts receivable.

Because collateral reduces lender risk, secured loans often provide lower interest rates, larger loan amounts, and longer repayment terms.

Unsecured Business Term Loans

Unsecured loans do not require physical collateral. Instead, lenders primarily evaluate credit score, business revenue, time in business, cash flow, and financial history.

These loans offer faster approval and fewer documentation requirements but may come with higher interest rates due to increased lender risk.

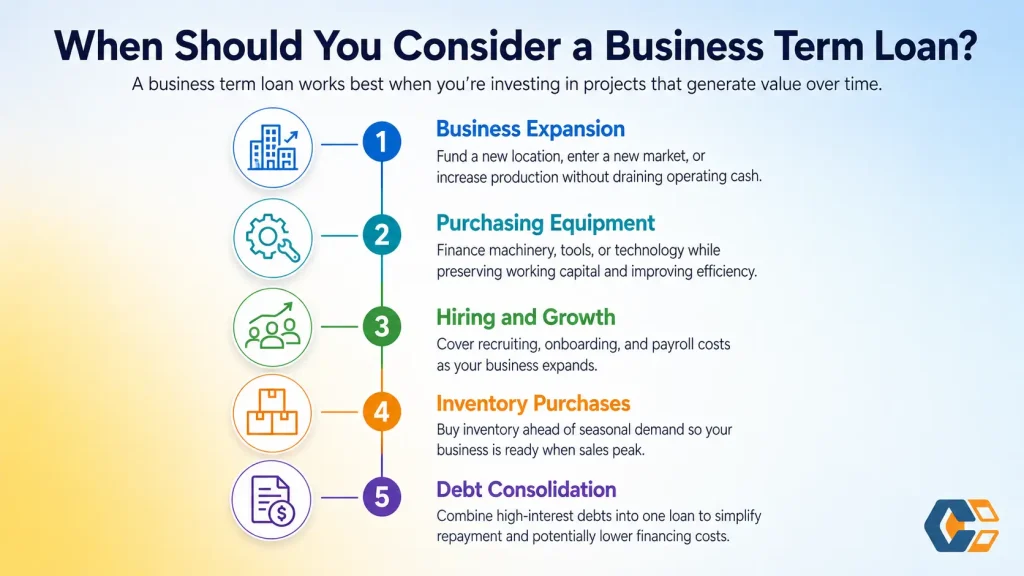

When Should You Consider a Business Term Loan?

A business term loan works best when you’re investing in projects that generate value over time.

Business Expansion

Opening a new location, entering a new market, or increasing production often requires significant upfront investment. A term loan provides the capital needed without draining operating cash. For businesses focused on expansion, this guide on using working capital to expand operations offers helpful context.

Purchasing Equipment

Whether you’re replacing outdated machinery or investing in new technology, financing equipment through a term loan allows you to preserve working capital while improving efficiency.

Hiring and Growth

As your business expands, you may need additional employees, specialized talent, or management staff. A term loan can help cover recruitment, onboarding, and payroll costs during growth periods.

Inventory Purchases

Businesses preparing for seasonal demand often need to increase inventory levels before sales begin. A term loan can finance these purchases so you’re ready when customer demand peaks.

Debt Consolidation

If your business has multiple high-interest debts, consolidating them into a single term loan may simplify repayment and potentially lower financing costs. For businesses currently carrying expensive financing, review refinancing high-cost business loans before making a decision.

Key Benefits of Business Term Loans

Business owners continue choosing term loans because they provide both stability and flexibility.

Predictable Monthly Payments

One of the biggest advantages is knowing exactly how much you’ll pay every month. This predictability supports better budgeting, easier forecasting, and improved cash flow management.

Competitive Interest Rates

Compared to credit cards, merchant cash advances, and many short-term financing options, business term loans often offer lower interest rates, particularly for borrowers with strong financial profiles.

Interest rates can change based on broader market conditions, so business owners should understand how inflation and interest rates affect small business loans before comparing offers.

Builds Business Credit

Making on-time payments helps establish a positive business credit history. A stronger credit profile may improve eligibility for larger loan amounts, lower interest rates, better financing options, and future lines of credit. Before applying, read these ways to improve your business credit score.

Flexible Loan Amounts

Business term loans are available in a wide range of funding amounts, allowing companies to borrow based on their actual needs rather than accepting a one-size-fits-all financing solution.

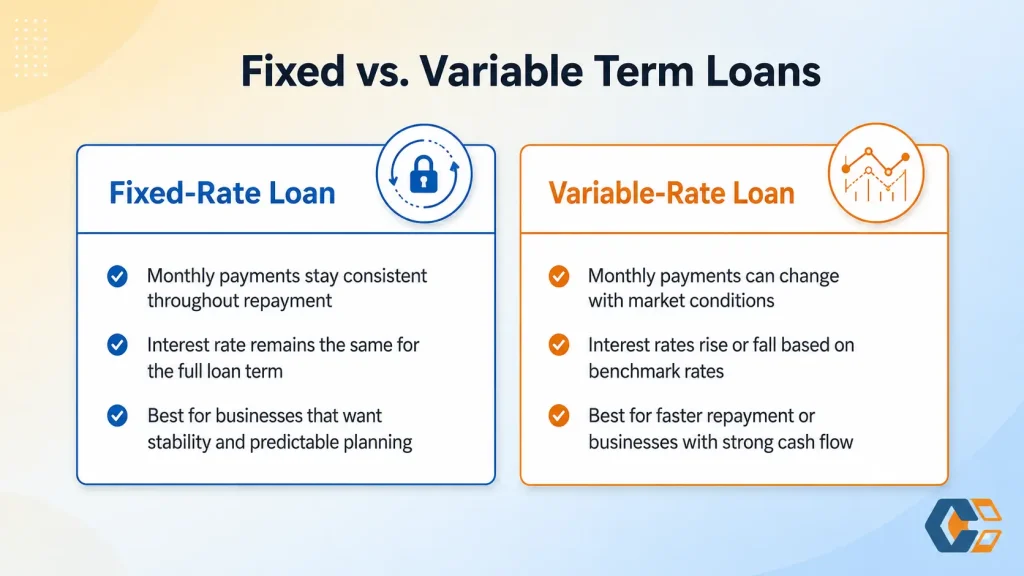

Fixed vs. Variable Interest Rate Business Term Loans

One of the most important decisions you’ll make when choosing a business term loan is whether to select a fixed or variable interest rate.

With a fixed-rate loan, your interest rate remains the same throughout the repayment period. As a result, your monthly payment stays consistent, making it easier to budget and forecast expenses.

Variable-rate loans have interest rates that can increase or decrease based on market conditions or a benchmark rate. They may offer lower initial rates, but if rates rise, your monthly payments could increase.

If your priority is predictable payments and long-term planning, a fixed-rate loan is often the better choice. A variable-rate loan may be worth considering if you expect to repay the loan quickly or your business has sufficient cash flow to manage payment fluctuations.

How to Qualify for a Business Term Loan

Qualification requirements vary by lender, but most lenders review similar financial factors to determine whether a business can repay the loan responsibly. To improve your chances of approval, your business should show stable revenue, organized financial records, and a clear ability to manage monthly payments.

Most lenders typically evaluate:

- Time in business: Many lenders prefer businesses with at least 6–12 months of operating history.

- Consistent revenue: Lenders look for steady monthly or annual revenue that shows your business can support loan payments.

- Credit score: A business or personal credit score of 600 or higher may improve approval chances, although requirements vary.

- Business bank statements: Recent bank statements help lenders review cash flow and deposit activity.

- Tax returns: Some lenders request business or personal tax returns to verify income.

- Profit and loss statements: These documents show revenue, expenses, and profitability.

- Balance sheets: A balance sheet helps lenders understand your assets, liabilities, and overall financial position.

- Identification and business documents: Lenders may request government-issued ID, business registration, licenses, or ownership documents.

- Existing debt obligations: Current loans or debt payments help lenders evaluate repayment capacity.

- Industry and cash flow: Some lenders consider your industry risk, seasonal trends, and overall cash flow stability.

Modern lending is also becoming more data-driven. Many lenders now use technology, automation, and risk models to review applications faster and evaluate borrower strength more accurately. For more insight, read how AI is changing small business loan underwriting.

Tips to Improve Your Approval Chances

Preparing before you apply can increase the likelihood of receiving favorable loan terms.

Maintain healthy credit, keep financial records organized, reduce existing debt, borrow only what you need, and work with financing specialists who understand lender requirements.

At Committed to Capital, we help businesses identify lending solutions that match their qualifications, reducing unnecessary applications and improving approval chances.

Common Reasons Business Loan Applications Are Denied

Common reasons include insufficient business revenue, limited operating history, poor credit history, incomplete documentation, excessive existing debt, irregular cash flow, and recent bankruptcies or collections.

If your application is not approved initially, improving these areas may increase your chances with future lenders.

Business Term Loan vs. Other Financing Options

A business term loan provides funds as one lump sum, includes a fixed repayment schedule, and is best for planned investments such as expansion, equipment, and major purchases.

A business line of credit allows you to access funds as needed up to an approved limit. It is often better for ongoing operating expenses, seasonal cash flow gaps, and short-term needs where the exact funding amount may change.

Invoice factoring may be useful when unpaid invoices are creating cash flow pressure. Learn more about how invoice factoring improves cash flow.

Revenue-based financing may also be an option for businesses with consistent sales but changing monthly revenue. This guide explains what revenue-based financing is and how it works.

For certain businesses, combining traditional financing with SBA-backed options may provide additional flexibility. Read more about combining SBA loans with traditional bank financing.

Common Mistakes to Avoid When Applying for a Business Term Loan

Choosing financing carefully can help you avoid unnecessary costs and repayment challenges.

Avoid borrowing more than necessary, ignoring the total cost of the loan, accepting the first offer without comparison, overlooking cash flow, or signing an agreement without understanding repayment terms.

For a deeper breakdown, read our guide on term loan mistakes small businesses should avoid.

Why Businesses Choose Committed to Capital

Finding financing should not be stressful or time-consuming.

At Committed to Capital, we simplify the lending process by helping business owners compare financing options that align with their goals.

Our approach focuses on transparency, speed, and personalized service.

We help business owners understand funding options, compare terms, and move forward with confidence. Local entrepreneurs can also review our guide on how small business loans work for additional context.

Conclusion

Business term loans offer a practical and reliable way for small and medium-sized businesses to access the capital needed for growth. Whether you’re purchasing equipment, expanding into new markets, increasing inventory, or strengthening working capital, a term loan provides the structure and predictability many businesses need to plan with confidence.

Understanding how business term loans work, the different loan types available, qualification requirements, and repayment options allows you to make informed borrowing decisions that support your long-term goals.

At Committed to Capital, we’re committed to making business financing straightforward. Our experienced funding specialists work closely with business owners to identify lending solutions that fit their unique needs, helping them move forward with confidence.

Ready to grow your business? Contact Committed to Capital today to explore business term loan options and take the next step toward achieving your goals.