Cash flow makes or breaks construction businesses. You win a project, but payroll, equipment, and material costs hit weeks before the client pays. That gap between spending and getting paid sinks more contractors than slow sales ever do. Construction business loans exist to close that gap, fund growth, and keep your crews working without draining your reserves.

This guide walks you through how construction financing actually works, the loan types worth knowing, how lenders evaluate you, and how to choose the right funding for your situation. Whether you run a two-person remodeling outfit or a growing general contracting firm, you’ll find practical direction here.

Why Construction Businesses Need Specialized Financing

Construction operates on a payment structure unlike most industries. You front the costs and wait. Progress payments, retainage held until project completion, and net-30 to net-90 client terms all stretch your working capital thin. A profitable company can still run out of cash mid-project simply because money goes out faster than it comes in.

On top of timing problems, the industry carries heavy upfront costs. Heavy equipment, specialized tools, bonding requirements, licensing, insurance, and skilled labor all demand capital before a single invoice gets paid. Seasonal swings add another layer, with winter slowdowns in many regions forcing contractors to stretch summer earnings across lean months.

Construction business loans address these realities directly. The right financing covers payroll during payment gaps, funds equipment purchases without wiping out savings, and gives you the capital to take on larger projects that grow your revenue.

Common Types of Construction Business Loans

Different problems call for different financing tools. Understanding what each loan does helps you match the solution to your actual need instead of taking whatever a lender pushes.

Term Loans

A term loan gives you a lump sum repaid over a fixed period with set monthly payments. This works well for major one-time investments like buying a large piece of equipment, expanding your facility, or acquiring another company. Banks, credit unions, and online lenders all offer term loans, with rates and terms depending heavily on your credit profile and business history.

Business Lines of Credit

A line of credit gives you a revolving pool of funds you draw from as needed and repay, then borrow against again. This flexibility makes it ideal for managing cash flow gaps, covering payroll between progress payments, or handling unexpected costs. You only pay interest on what you actually use, which makes it far more efficient than a lump sum for ongoing needs.

Equipment Financing

Equipment financing lets you buy machinery, vehicles, or tools with the equipment itself serving as collateral. Because the asset secures the loan, approval tends to be easier and rates more favorable than unsecured options. Excavators, loaders, dump trucks, and specialized tools all qualify, and you spread the cost over the useful life of the asset rather than paying everything upfront.

SBA Loans

The U.S. Small Business Administration backs loans through approved lenders, reducing risk for the bank and opening doors for borrowers who might not qualify otherwise. SBA 7(a) loans offer general-purpose funding up to $5 million, while SBA 504 loans target major fixed assets like real estate and heavy equipment. These loans carry competitive rates and long repayment terms, though the application process takes longer and demands more documentation.

Invoice Factoring

When clients owe you money but haven’t paid, invoice factoring turns those outstanding invoices into immediate cash. You sell unpaid invoices to a factoring company at a discount and receive most of the value upfront. This solves the classic construction problem of completed work tied up in slow-paying receivables, though it costs more than traditional borrowing.

Working Capital Loans

Working capital loans provide short-term funding to cover everyday operating expenses during slow periods or rapid growth. They bridge the gap when revenue lags behind obligations, keeping your operation running smoothly through seasonal dips or expansion phases.

Construction Business Loan Types at a Glance

| Loan Type | Best For | Typical Use Case | Collateral |

| Term Loan | Large one-time investments | Facility expansion, acquisitions | Sometimes required |

| Business Line of Credit | Ongoing cash flow gaps | Payroll between progress payments | Often unsecured |

| Equipment Financing | Buying machinery or vehicles | Excavators, dump trucks, tools | The equipment itself |

| SBA Loan (7a / 504) | Long-term growth & real estate | Up to $5M for major investments | Varies by program |

| Invoice Factoring | Slow-paying receivables | Turning unpaid invoices into cash | The invoices |

| Working Capital Loan | Short-term operating costs | Seasonal slowdowns, rapid growth | Often unsecured |

Get Construction Financing Built Around the Way You Work

You don’t have time to chase banks while your crews wait on payroll. Committed to Capital delivers fast, flexible funding designed around real cash flow, with decisions in 24 to 48 hours and no collateral required.

From equipment financing and lines of credit to SBA 7(a) and 504 loans, we match contractors with the right capital from $10K to $5M. With over $50 million funded and a dedicated advisor on every account, you get real human support, not red tape.

Check your funding options in a few minutes, with no credit impact and no obligation.

How Lenders Evaluate Construction Businesses

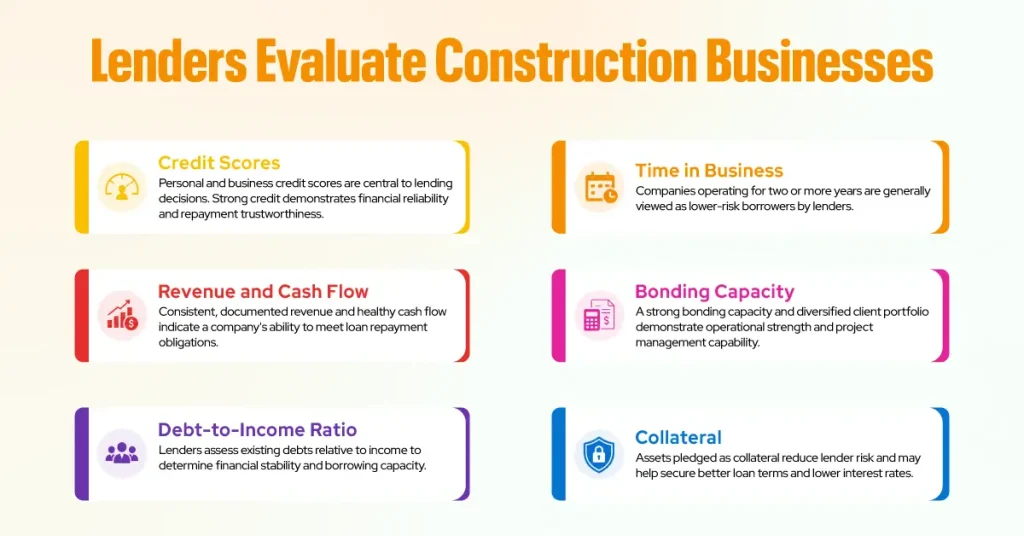

Lenders assess risk before they lend, and construction carries a reputation for volatility. Knowing what they examine helps you strengthen your application before you apply.

Your personal and business credit scores sit at the center of most decisions. Strong credit signals reliability and unlocks better rates. Lenders also scrutinize your time in business, since companies operating two or more years present lower risk than startups. Your annual revenue and cash flow demonstrate whether you can handle repayment, so consistent, documented income strengthens your case significantly.

Beyond the numbers, lenders look at your debt-to-income ratio, existing obligations, and the health of your project pipeline. A backlog of signed contracts shows future revenue and reassures lenders that work keeps coming. Some will also weigh your bonding capacity and the diversity of your client base, since dependence on a single major client raises risk.

Collateral matters too. Secured loans backed by equipment, real estate, or other assets typically come with lower rates and higher approval odds than unsecured financing.

What Lenders Look For and How to Strengthen Each Factor

| Evaluation Factor | What Lenders Want | How to Improve It |

| Credit Score | 680+ for banks, 600s for online lenders | Pay debts on time, fix report errors |

| Time in Business | 2+ years preferred | Document consistent operating history |

| Annual Revenue | Steady, verifiable income | Keep clean profit and loss statements |

| Debt-to-Income Ratio | Lower is better | Pay down existing debt before applying |

| Project Pipeline | Signed contracts and backlog | Show future revenue from current jobs |

| Collateral | Equipment, real estate, receivables | Identify assets you can pledge |

How to Choose the Right Financing for Your Situation

Start by defining the problem you’re solving. Matching the loan to the need prevents you from paying for the wrong tool.

If you face short-term cash flow gaps, a line of credit or invoice factoring usually fits best because both address timing rather than long-term investment. For major equipment purchases, equipment financing keeps your cash free while spreading the cost across the asset’s lifespan. When you’re funding genuine expansion, such as a new location or a business acquisition, a term loan or SBA loan provides the larger, longer-term capital those moves require.

Next, weigh the true cost of borrowing. Look past the advertised rate to the annual percentage rate (APR), which captures fees alongside interest. Compare repayment terms, prepayment penalties, and any origination charges. A loan with a low rate but heavy fees can cost more than a slightly higher-rate option with cleaner terms.

Finally, consider speed and qualification requirements honestly. Online lenders fund fast but charge more. Banks and SBA loans cost less but move slowly and demand stronger credentials. Choose based on how quickly you need the money and how strong your financials are right now.

Match Your Need to the Right Financing Tool

| Your Situation | Recommended Financing | Why It Fits |

| Cash flow gap before client pays | Line of credit or invoice factoring | Solves timing, not long-term debt |

| Buying heavy equipment | Equipment financing | Asset secures the loan, keeps cash free |

| Opening a new location | Term loan or SBA loan | Larger, longer-term capital |

| Covering a seasonal slowdown | Working capital loan | Bridges revenue dips |

| Acquiring another company | SBA 7(a) loan | Up to $5M with long repayment terms |

| Need funds within days | Online lender or revenue-based financing | Fast approval and funding |

Steps to Apply for a Construction Business Loan

Preparation separates approved applications from rejected ones. Lenders reward contractors who come ready.

Begin by gathering your documentation. Most lenders want business and personal tax returns, bank statements, profit and loss statements, balance sheets, and a list of current contracts or your project pipeline. Having these organized before you apply speeds up the process and signals professionalism.

Check your credit reports next and correct any errors that could drag down your score. Then determine exactly how much you need and how you’ll use it, since a clear, specific funding purpose strengthens your application far more than a vague request.

Research lenders that specialize in construction or small business lending, and compare multiple offers rather than accepting the first approval. Once you’ve chosen, submit a complete application with all supporting documents. Respond quickly to follow-up requests, because delays on your end stall the entire process.

Fund Your Next Project With Committed to Capital

The right financing turns cash flow gaps into growth opportunities. Trusted by 500+ U.S. businesses across construction, logistics, and beyond, Committed to Capital pairs you with real offers from top-tier lenders aligned with your goals, with most clients funded within one to two business days.

Whether you’re covering a payroll gap, financing heavy equipment, or taking on a larger job, our advisors help you find the structure that fits your business cycles. Based in Pitman, New Jersey, and serving contractors nationwide.

Start your application today, it takes about 60 seconds.

Tips to Improve Your Approval Odds

Strengthening your position before you apply pays off in better terms and higher approval rates. Build and maintain strong business credit by paying vendors and existing debts on time and keeping credit utilization low. Separate your business and personal finances completely, since commingled accounts complicate underwriting and weaken your profile.

Keep clean, current financial records year-round rather than scrambling at application time. Maintain a healthy cash reserve, because lenders favor borrowers who aren’t desperate. Reducing existing debt before applying improves your debt-to-income ratio and your appeal. Finally, build relationships with lenders before you need money, since an established banking relationship often smooths approval when the time comes.