For New Jersey business owners, access to capital can make the difference between staying stuck and moving into a stronger stage of growth. Whether you run a contractor business in Newark, a medical practice near Morristown, a restaurant in Jersey City, a logistics company along the Turnpike corridor, or a retail shop on the Jersey Shore, lenders want to see more than revenue. They want proof that your business can manage debt responsibly.

Key Takeaways

- Check your business credit reports before applying for capital. Review your business profiles for errors, outdated information, missing trade lines, and inconsistent business details.

- Pay vendors and lenders on time or early. Strong payment history is one of the most important factors lenders review when evaluating business creditworthiness.

- Use trade lines that report to business credit bureaus. Vendor accounts, supplier terms, business credit cards, and other reporting accounts can help build a stronger business credit profile.

- Lower credit utilization before submitting a funding application. Paying down balances on business credit cards and lines of credit can make your company look less risky to lenders.

- Prepare your business before applying for New Jersey capital. Clean financial records, separated business finances, resolved past-due accounts, and organized documents can improve lender confidence.

A strong business credit score can help you qualify for better financing terms, larger credit limits, lower rates, and more lender confidence. Business credit scores are commonly used by lenders, suppliers, vendors, insurance companies, and potential partners to evaluate risk.

Before applying for a business loan, Line of Credit, Equipment Financing, working capital, SBA-backed financing, or a New Jersey small business funding program, it is worth taking time to strengthen your business credit. Here are seven practical ways to improve your business credit score before applying for capital in New Jersey.

1. Review Your Business Credit Reports Before a Lender Does

The first step is simple: Know what lenders may see before you submit an application. Many business owners focus only on their personal credit score, but commercial lenders may also review business credit reports from agencies such as Dun & Bradstreet, Experian Business, and Equifax Business.

Your business credit report may include payment history, public records, collections, outstanding debts, industry classification, business age, credit utilization, and reported vendor relationships. If there are errors, outdated balances, duplicate accounts, incorrect addresses, or missing payment data, those details could weaken your application.

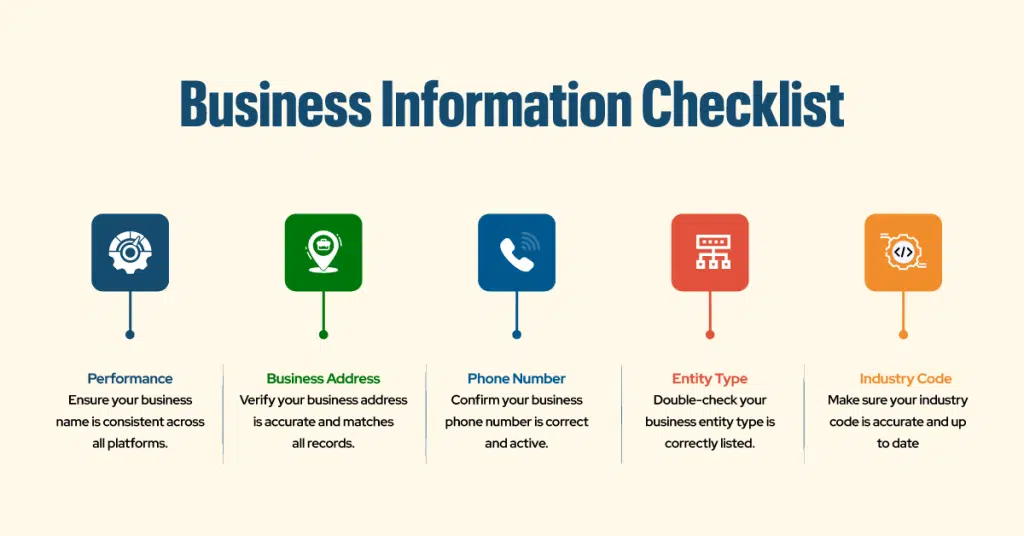

Before applying for capital, check your business name, address, phone number, entity type, and industry code across every major profile. Your information should match your New Jersey business registration, tax records, bank account, website, insurance documents, and financing application. Even small inconsistencies can create delays or make your business look less established.

If you find inaccurate information, file disputes directly with the reporting bureau. Also contact vendors or creditors that may have reported incorrect data. Cleaning up your profile early gives you more control before a lender reviews your file.

2. Pay Vendors, Lenders, and Suppliers On Time or Early

Payment history is one of the most important parts of business credit. If your company regularly pays late, your score can suffer. If your company pays on time or early, your profile becomes more attractive to lenders.

For New Jersey businesses, this applies to many common relationships: wholesalers, construction material suppliers, restaurant distributors, office supply vendors, commercial landlords, insurance providers, fleet service companies, and professional service providers.

If those accounts report to a business credit bureau, your payment timing may help or hurt your profile. It’s worth noting that how AI evaluates creditworthiness is changing this picture, since many modern lenders now weigh alternative data like cash flow and payment behavior alongside your traditional credit score.

A good habit is to pay invoices before the due date whenever cash flow allows. If your vendor terms are net 30, try to pay by day 20 or 25. If your business has seasonal swings, such as a tourism company near Cape May, a landscaping business in Bergen County, or a retail shop near the boardwalk, build a payment calendar so bills do not get missed during slower months.

Automated reminders, accounting software, and weekly payables reviews can also help. The goal is to build a consistent record that says your business pays as agreed.

Ready to Improve Your Business Credit Before Applying for Capital?

Committed to Capital helps New Jersey business owners prepare for funding with confidence. If you are planning to apply for working capital, a business line of credit, equipment financing, or growth funding, strengthening your business credit profile first can improve your chances of finding the right financing option.

Our team helps business owners understand what lenders look for, organize key financial documents, and move toward capital readiness with a clearer strategy.

3. Open Trade Lines That Report to Business Credit Bureaus

Many small businesses pay vendors on time but still have thin business credit files because their vendors do not report payment history. A lender cannot reward positive payment behavior it cannot see.

To improve your business credit score, work with vendors, suppliers, or business credit cards that report to commercial credit bureaus. These reporting trade lines can help establish a stronger credit history for your company.

This is especially important for younger New Jersey businesses that have strong revenue but limited credit depth. A two-year-old HVAC company in Edison, a boutique in Hoboken, or a home health care provider in Cherry Hill may have solid operations but still appear risky if there are too few accounts on file.

Start with manageable accounts. You may consider office supplies, fuel cards, shipping accounts, inventory vendors, or industry-specific suppliers that extend net terms. Use the accounts responsibly and pay on time. Over time, these trade lines may help build a more complete profile.

Do not open accounts simply to create activity. Open accounts that serve a real business purpose. Lenders want to see responsible financial behavior, not unnecessary debt.

4. Lower Credit Utilization and Avoid Maxing Out Business Accounts

Credit utilization refers to how much available credit your business is using. If your company has a $50,000 business line of credit and consistently carries a $48,000 balance, lenders may see that as a warning sign. Even if you make payments on time, high utilization can suggest cash flow pressure.

Before applying for capital, review your balances on business credit cards, lines of credit, charge accounts, and vendor accounts. If possible, pay down revolving balances before submitting your application.

This can be especially useful before applying for larger financing, such as equipment funding, expansion capital, or a working capital loan. A lender reviewing your business may want to see that you have room in your existing credit facilities and are not relying too heavily on short-term debt.

For example, a trucking company near Port Newark may need capital for repairs or fleet expansion. A restaurant in Montclair may need a line of credit before patio season. A medical office in Princeton may want financing for new equipment. In each case, lower utilization can make the business appear more stable.

Strong credit management shows lenders that your company can handle additional capital without becoming overextended.

5. Separate Business and Personal Finances Clearly

A business credit score is easier to build when your business is treated as a separate financial entity. That means using a business bank account, business credit accounts, business insurance, proper bookkeeping, and consistent legal documentation.

| Section | Keep Your Business and Personal Finances Separate |

| Main Idea | A business credit score is easier to build when your company is treated as a separate financial entity. This means using business-only accounts, records, and documentation. |

| What to Use | Use a dedicated business bank account, business credit accounts, business insurance, proper bookkeeping, and consistent legal documents. |

| Why It Matters | Mixing personal and business expenses can make it harder for lenders to understand your company’s true financial health. It may also make your business appear less professional or less established. |

| New Jersey Business Tip | New Jersey business owners should make sure their business entity is properly registered, their EIN is used consistently, and their business address is accurate across all records. |

| Where Information Should Match | Your business name and details should appear consistently on bank statements, tax filings, insurance policies, invoices, licenses, your website, and business credit profiles. |

| How It Helps With Financing | Lenders often review bank statements, profit and loss statements, balance sheets, tax returns, and debt schedules. Clean financial separation makes the underwriting process easier and can improve lender confidence. |

| Personal Credit Reminder | Personal credit may still matter, especially for newer businesses or financing that requires a personal guarantee. Some lenders may review both business and owner-related credit information. |

| Final Takeaway | Protecting both your business and personal credit can strengthen your funding application before applying for capital. |

6. Resolve Collections, Liens, Judgments, and Past-Due Accounts

Negative public records and collection accounts can seriously damage lender confidence. Before applying for capital, search for unresolved issues that may appear in your business credit profile or public records.

This may include tax liens, unpaid vendor balances, collection accounts, judgments, or old accounts that were never properly closed. Even if the issue is small, it can create concern during underwriting.

New Jersey businesses should be especially careful with state tax compliance, payroll obligations, sales tax filings, and industry-specific licensing requirements. A lender wants to know that your business is not carrying hidden liabilities that could interfere with repayment.

If you have past-due accounts, contact the creditor and ask about bringing the account current, negotiating a payoff, or correcting inaccurate reporting. If a lien or judgment has already been satisfied, make sure the record reflects that. Documentation matters. Keep proof of payment, settlement letters, release documents, and updated account statements.

Do not ignore old issues and hope they will go unnoticed. Lenders are often better at finding problems than borrowers expect. It is better to address them before you apply.

7. Build a Strong Capital-Readiness File Before Applying

Improving your business credit score is not only about the score itself. It is also about making your business look prepared, organized, and fundable.

Before applying for capital in New Jersey, create a capital-readiness file that includes your recent bank statements, tax returns, profit and loss statement, balance sheet, debt schedule, business plan or use-of-funds summary, entity documents, lease agreement, insurance documents, and key licenses. If you are applying for equipment financing, include quotes or invoices. If you are applying for expansion capital, include projections and a clear explanation of how the funding will support revenue.

This preparation helps lenders see the full picture. A business credit score may open the door, but clean documentation can help move the application forward.

It is also important to match the financing product to your business needs. A short-term working capital product may be useful for inventory or temporary cash flow gaps. A term loan may fit a larger expansion. A business line of credit may help with flexible, recurring needs. Equipment financing may be better for vehicles, machinery, kitchen equipment, medical devices, or construction tools.

In New Jersey, where business costs can vary significantly between areas such as Jersey City, Newark, Trenton, Atlantic City, and suburban markets, lenders may want to understand how your business model works locally. Be ready to explain your customer base, location, revenue trends, seasonality, and competitive advantage.

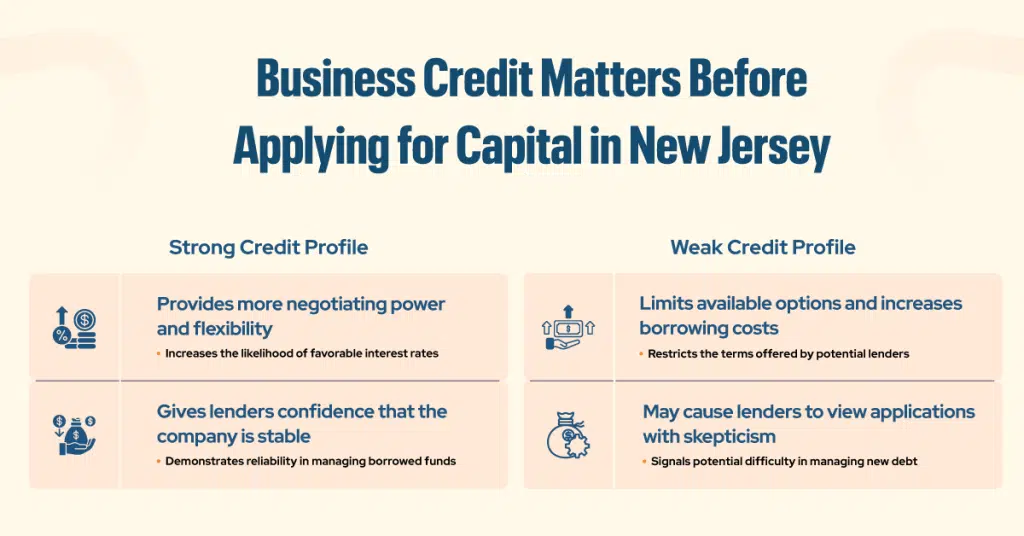

Why Business Credit Matters Before Applying for Capital in New Jersey

New Jersey has a dense and competitive business environment. Companies often deal with high operating costs, commercial rents, payroll demands, insurance expenses, transportation costs, and seasonal revenue shifts. A strong business credit profile can give lenders more confidence that your company is stable enough to manage funding.

Your score is not the only factor. Lenders may also consider revenue, time in business, cash flow, industry, collateral, existing debt, tax compliance, personal credit, and the purpose of the funds. But business credit can influence how your application is viewed, what terms you receive, and how much capital may be available.

A weak credit profile does not always mean you cannot get funding. However, it may limit your options or increase your borrowing costs. A stronger profile gives you more negotiating power and more flexibility.

How Long Does It Take to Improve a Business Credit Score?

The timeline depends on your starting point. Some improvements, such as correcting inaccurate information or paying down revolving balances, may help relatively quickly once updates are reported. Other improvements, such as building new trade lines and establishing a longer payment history, can take several months or more.

That is why the best time to work on business credit is before you urgently need capital. Waiting until payroll is due, equipment breaks, inventory runs low, or a lease opportunity appears can leave you with fewer options.

Ideally, review your business credit at least three to six months before applying for funding. If you know you want capital later this year, start now.

Get Capital-Ready with Committed to Capital

Before you apply for business funding, make sure your credit, cash flow, and financial records are working in your favor. Committed to Capital supports New Jersey businesses by helping them identify funding opportunities, prepare stronger applications, and avoid common mistakes that can delay approval. Whether you are growing, stabilizing cash flow, buying equipment, or preparing for your next opportunity.

We can help you take the next step toward responsible business financing.

Bottom Line

Improving your business credit score before applying for capital in New Jersey is one of the smartest steps you can take as a business owner. It shows lenders that your company is organized, responsible, and ready to manage financing.

Start by reviewing your credit reports, correcting errors, paying vendors early, adding reporting trade lines, lowering utilization, separating business and personal finances, resolving negative records, and preparing strong financial documents. These steps can help you build credibility before your application reaches a lender’s desk.

For New Jersey businesses, capital readiness is not just about getting approved. It is about qualifying for the right funding at the right time with terms that support long-term growth.