Inflation and interest rates are two of the biggest forces shaping how small businesses borrow money. For Delaware business owners, from restaurants in Wilmington and Newark to contractors in Dover, retailers in Rehoboth Beach, and service companies across Sussex County, rising costs can quickly change the way financing decisions are made.

When inflation increases, the cost of goods, materials, payroll, rent, insurance, equipment, and everyday operations often rises with it. At the same time, lenders may adjust business loan rates to reflect broader market conditions. That means a loan that looked affordable last year may carry a higher monthly payment today, and a business that once had strong cash flow may need to review its borrowing strategy more carefully.

Understanding how inflation and interest rates work together can help Delaware small business owners make smarter financing choices, protect cash flow, and avoid taking on debt that does not support long-term growth.

What Inflation Means for Delaware Small Businesses

Inflation happens when the overall cost of goods and services rises over time. For small businesses, inflation is not just an economic headline. It shows up in the price of inventory, fuel, construction materials, food supplies, utilities, rent, wages, and vendor contracts.

A Delaware café in Trolley Square may pay more for ingredients and packaging. A landscaping company in Middletown may face higher fuel and equipment costs. A boutique near the Rehoboth Beach Boardwalk may need to spend more on wholesale products before the busy tourism season. Even professional service businesses in Wilmington can feel inflation through higher software, insurance, office, and payroll expenses.

These rising costs put pressure on working capital. When more money is going out each month, businesses may have less cash available for payroll, marketing, expansion, or debt payments. This is where business financing can help, but inflation also affects the cost and structure of loans.

How Interest Rates Affect Small Business Loans

Interest rates determine how much a business pays to borrow money. When rates rise, the cost of financing usually rises too. This can affect term loans, business lines of credit, SBA loans, equipment financing, commercial real estate loans, and other funding products.

The Federal Reserve often raises interest rates to help slow inflation. As borrowing becomes more expensive, lenders typically pass those higher costs to borrowers through higher loan rates, tighter approval standards, or shorter repayment terms.

For Delaware small businesses, this means timing matters. A business owner who waits too long to secure financing may face higher payments later. On the other hand, rushing into the wrong loan can create unnecessary financial strain. The goal is to match the loan type, repayment term, and rate structure to the business’s real cash flow needs.

Fixed-Rate vs. Variable-Rate Loans During Inflation

During inflation, choosing between fixed-rate and variable-rate financing affects payment stability, borrowing flexibility, and long-term planning for Delaware small businesses.

| Loan Type | Main Benefit | Possible Risk | Best For |

| Fixed-Rate Loan | Predictable monthly payments make budgeting easier when other business costs are rising. | The starting rate may be higher than some variable-rate options. | Equipment purchases, renovations, expansion projects, and long-term investments. |

| Variable-Rate Loan | May offer flexibility and sometimes starts with a lower initial rate. | Payments can increase if interest rates rise, making cash flow less predictable. | Short-term funding needs, business lines of credit, inventory purchases, and temporary working capital. |

| Delaware Business Example | Each option can support growth when matched to the right business need. | Rising rates can increase borrowing costs for variable-rate loans. | A Dover contractor may use a variable-rate line of credit for materials, while a New Castle manufacturer may choose fixed-rate equipment financing. |

| Key Decision Factor | Helps business owners align financing with their operating needs. | Choosing the wrong structure can create unnecessary financial pressure. | Businesses should choose based on repayment timeline, cash flow, and ability to handle payment changes. |

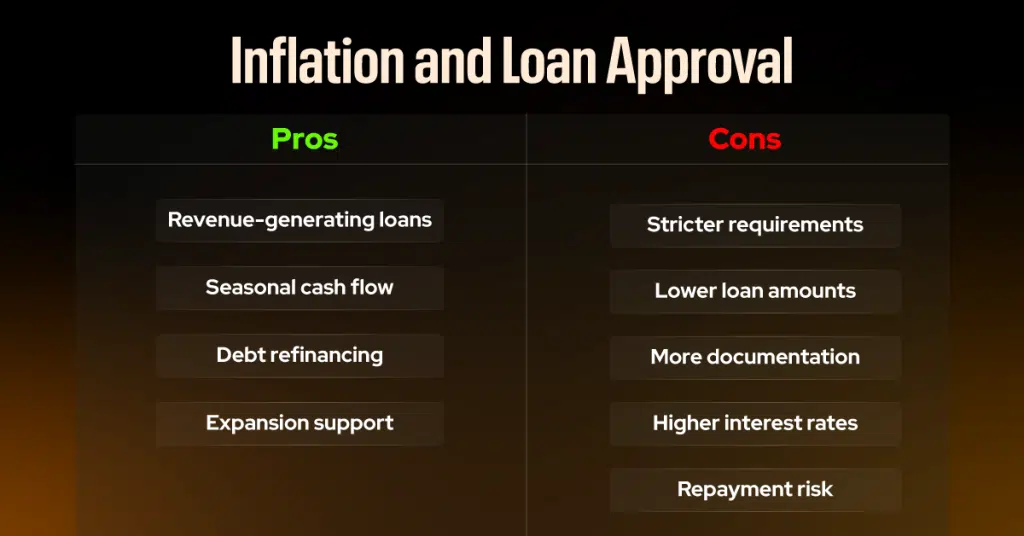

Why Inflation Can Make Loan Approval More Difficult

Inflation does not only affect loan rates. It can also affect loan approval.

When costs rise, lenders may look more closely at a business’s cash flow, profit margins, credit profile, and existing debt. If a company’s expenses are growing faster than revenue, lenders may see more repayment risk. This can lead to stricter requirements, lower approved loan amounts, more documentation, or higher rates.

Delaware business owners can improve their chances of approval by preparing before they apply. Clean financial statements, updated profit and loss reports, business bank statements, tax returns, and a clear explanation of how the loan will be used can make a strong difference.

Lenders want to see that the business has a plan. A loan used to purchase revenue-generating equipment, stabilize seasonal cash flow, refinance expensive debt, or support a profitable expansion may be viewed more favorably than a loan requested without a clear purpose.

How Rising Rates Impact Monthly Payments

Higher interest rates can significantly change monthly loan payments. Even a small rate increase may affect affordability, especially on larger loans or longer repayment terms.

For example, a Delaware business borrowing for equipment, renovations, inventory, or working capital should not only ask, “Can I qualify?” The better question is, “Can my business comfortably repay this loan while still covering payroll, rent, taxes, inventory, and operating expenses?”

This is especially important for businesses with seasonal revenue. Coastal businesses in Lewes, Bethany Beach, Dewey Beach, and Rehoboth Beach may earn a large share of revenue during the summer season. If loan payments are too high during slower months, cash flow can become tight even if the business is profitable overall.

Before accepting financing, business owners should review the full repayment amount, payment frequency, fees, prepayment terms, and whether the rate is fixed or variable.

Common Loan Options for Delaware Small Businesses

Different loan products respond differently to inflation and interest rate changes. Choosing the right one can help Delaware small business owners reduce risk, protect cash flow, and borrow with more confidence.

Term loans: Term loans are often used for larger investments, business expansion, refinancing, or working capital. They usually provide a lump sum that is repaid through scheduled payments over time. Fixed-rate term loans can offer stability when interest rates are uncertain.

Pros: Predictable repayment structure and useful for major business investments.

Cons: May require strong credit, documentation, and consistent cash flow.

Business lines of credit: Business lines of credit are useful for short-term cash flow needs, inventory purchases, emergency expenses, or seasonal gaps. They provide flexible access to funds, allowing business owners to draw only what they need.

Pros: Flexible funding and helpful for managing temporary cash flow challenges.

Cons: Many lines of credit have variable rates, so borrowing costs can rise when interest rates increase.

SBA loans: SBA loans may offer competitive terms for qualified businesses. They can be useful for long-term financing, business acquisition, working capital, equipment, or commercial real estate.

Pros: Often provide favorable repayment terms and lower down payment options for eligible borrowers.

Cons: The application process may require more paperwork and take longer than other financing options.

Equipment financing: Equipment financing can help businesses purchase vehicles, machinery, kitchen equipment, medical equipment, or technology without paying the full cost upfront. Since the equipment often serves as collateral, this can be a practical choice for companies investing in productivity.

Pros: Helps preserve cash while allowing businesses to access needed equipment.

Cons: The financing is usually tied to the equipment, which may lose value over time.

Invoice financing: Invoice financing may help businesses that are waiting on unpaid invoices. This can be useful for companies that serve commercial clients, government contracts, or larger accounts with longer payment timelines.

Pros: Can improve cash flow without waiting for customers to pay invoices.

Cons: Fees can reduce profit margins, and approval may depend on the quality of customer invoices.

When Borrowing Still Makes Sense During Inflation

Higher rates do not always mean a business should avoid borrowing. In many cases, financing can still be a smart move if the loan supports growth, protects cash flow, or helps the business avoid bigger costs later.

Borrowing may make sense when the funds are used to purchase equipment that increases revenue, buy inventory before prices rise further, refinance expensive debt, cover seasonal working capital needs, or support a clear expansion opportunity.

For example, a Delaware restaurant that needs a new walk-in cooler may not be able to wait until prices drop. A construction company may need reliable vehicles or equipment to take on larger projects. A retail business may need inventory ahead of a busy season. In these cases, the cost of not investing may be higher than the cost of financing.

The key is to calculate the expected return. If borrowed capital helps the business generate more revenue, reduce costs, or improve efficiency, the loan may still be worthwhile even in a higher-rate environment.

How Delaware Businesses Can Prepare Before Applying

Preparation can help small business owners secure better financing options. Before applying for a loan, review your current cash flow, update your financial records, and identify the exact purpose of the funding.

It is also wise to compare loan products instead of focusing only on the interest rate. The lowest rate is not always the best deal if the repayment term is too short, fees are high, or the payment structure does not match your revenue cycle.

- Review your existing debt:

Business owners should look closely at high-interest debt, merchant cash advances, or variable-rate obligations before applying for new financing. - Consider refinancing when appropriate:

Refinancing may help simplify payments or improve cash flow, but it should be reviewed carefully to make sure the new loan lowers total costs or creates a better repayment structure. - Build a clear funding strategy:

For local businesses across Wilmington, Dover, Newark, Milford, Smyrna, and the Delaware beach communities, having a clear funding strategy can make borrowing less stressful and more effective. - Match financing to your business needs:

The right loan should support your cash flow, repayment ability, and long-term business goals rather than creating unnecessary financial pressure.

Committed to Capital: Flexible Small Business Financing for Delaware Entrepreneurs

At Committed to Capital, we help Delaware small business owners find financing solutions that fit their goals, cash flow, and growth plans. Whether you need working capital to manage rising costs, equipment financing to keep operations moving, or funding to expand your business, our team is here to make the process simple, clear, and supportive.

Do not let inflation or changing interest rates stop your next move. Connect with Committed to Capital today and explore funding options designed to help your business move forward with confidence.

Smart Loan Strategies in a Changing Economy

Inflation and interest rates will always move over time, but your business loan strategy should not be based on guesswork. A strong financing decision starts with understanding your numbers, knowing how rates affect repayment, and choosing a loan that supports your business instead of straining it.

Delaware small businesses operate in a diverse economy that includes tourism, construction, healthcare, retail, logistics, restaurants, agriculture, professional services, and manufacturing. Each industry feels inflation differently, which means each business needs a financing approach built around its own revenue cycle and operating costs.

The best approach is proactive. Review your cash flow before you are in a crunch. Explore financing before a major expense becomes urgent. Compare loan structures before choosing the fastest option. When business owners plan ahead, they are more likely to secure capital that helps them grow instead of creating unnecessary pressure.

Final Thoughts

Inflation and interest rates can have a major impact on small business loans in Delaware. Rising costs can reduce cash flow, while higher interest rates can make borrowing more expensive. At the same time, the right financing can help a business stay stable, invest in growth, and manage uncertainty.

The most important step is to borrow with a purpose. Know why you need the capital, how it will support your business, and how the repayment fits into your cash flow. With the right plan and the right financing partner, Delaware small business owners can make confident funding decisions even when the economy feels unpredictable.