Manufacturing Business Loans give factory owners the capital to buy equipment, expand facilities, stock raw materials, and bridge the cash gap between production costs and customer payments. In 2026, this financing became dramatically more affordable for U.S. manufacturers because the Small Business Administration waived most upfront fees and launched the first loan program built exclusively for the sector. If you run a factory, a metal shop, a food production line, or any business that transforms materials into finished goods, the funding landscape right now is the strongest it has been in a decade.

This guide walks you through every realistic financing option, what each one costs, how to qualify, and how to match the right loan to the right need. The goal is practical clarity: by the end, you will know which product fits your situation, what lenders look for, and how to avoid the expensive mistakes that trap unprepared borrowers.

Why Manufacturing Financing Works Differently Than Other Business Loans

Manufacturing carries a capital structure that most other industries never face. A retailer buys inventory and sells it within weeks. A service firm bills for time. A factory, by contrast, sinks enormous sums into machinery, tooling, and raw materials long before a single finished unit ships, and then often waits 30 to 90 days for customers to pay invoices. That timing gap defines the entire financing challenge. The same dynamic shapes other equipment-heavy fields, as our construction business loan guide explains for contractors facing similar cash flow pressure.

Because of this, manufacturers usually need several types of capital working together rather than a single loan. Equipment financing covers the CNC machines, presses, and robotics on the production floor. Real estate loans fund the building itself. Working capital lines cover payroll and raw materials during the production cycle.

Invoice factoring unlocks cash trapped in unpaid receivables. A well-structured manufacturer rarely relies on one product; it layers them so each dollar matches the asset or expense it supports.

Lenders also evaluate manufacturers through a specific lens. They look closely at machinery as collateral because industrial equipment holds resale value, they scrutinize customer concentration because losing one major buyer can sink a production schedule, and they weigh the debt service coverage ratio (DSCR) to confirm cash flow can comfortably absorb the new payment. Understanding how lenders think is the first step toward getting approved on favorable terms.

Get Matched With the Right Manufacturing Loan – Talk to Committed to Capital

Before you commit to any single product, it pays to see the full range of options side by side. Committed to Capital specializes in helping manufacturers structure financing that actually fits the way factories operate, from equipment acquisition and facility expansion to working capital and invoice-based funding. Rather than forcing your business into one rigid loan, the team helps you compare programs, layer the right products, and move quickly so production never stalls waiting on capital.

If you want a clear, no-pressure assessment of what your manufacturing business can qualify for, reach out to Committed to Capital here and start the conversation.

The Main Types of Manufacturing Business Loans

Manufacturers have access to a broad menu of financing, and each option solves a different problem. The sections below break down the products that matter most, what they fund, and when each one makes sense.

1. SBA Loans for Manufacturers (7a, 504, and the New MARC Program)

SBA loans are government-guaranteed financing delivered through approved lenders, and they offer some of the lowest rates and longest terms available to small manufacturers. In fiscal year 2026, the SBA made these loans exceptionally attractive for the sector. For 7(a) manufacturing loans of up to $950,000, the upfront fee is 0%, and for all 504 manufacturing loans, both the upfront fee and the annual service fee are 0%, effective from October 1, 2025 through September 30, 2026.

The SBA 7(a) loan is the most flexible option, supporting working capital, equipment, inventory, payroll, and debt refinancing. The 7(a) loan supports short-term and operational needs like payroll, inventory and product line expansion, especially where traditional financing falls short. The SBA 504 loan, by contrast, is built for major fixed assets.

The 504 program provides long-term, fixed-rate financing of up to $5.5 million for major fixed assets, including long-term machinery and equipment with a useful remaining life of a minimum of 10 years. Many manufacturers get the best of both worlds by combining SBA loans with traditional financing, pairing government-backed terms with conventional bank capital to cover a larger project.

The biggest 2026 development is a brand-new program built only for factories. The SBA MARC (Manufacturers’ Access to Revolving Credit) program launched in October 2025 as the first-ever manufacturer-specific SBA loan program, providing up to $5M in revolving working capital exclusively for manufacturers under NAICS codes 31-33.

Unlike a term loan, MARC functions like a credit line you draw from as needed for inventory, raw materials, and payroll, which maps perfectly to the production cycle. On top of these programs, legislation has expanded borrowing power significantly. The Made in America Manufacturing Finance Act, introduced in May 2025, doubled SBA loan caps for qualifying manufacturers from $5 million to $10 million on both the 7(a) and 504 programs.

2. Equipment Financing and Leasing

Equipment Financing is a loan or lease used specifically to purchase production machinery, where the equipment itself secures the debt. Because the lender can repossess the asset if you default, rates run lower than unsecured borrowing. This is the workhorse product for factory floors, covering everything from a single CNC machine to a fully automated production line.

In the current market, manufacturers are seeing strong terms. Manufacturing businesses can typically secure equipment loans at rates between 6% and 12% APR from conventional lenders. Approval and funding speed have also improved sharply. Lenders are offering 100% financing on modern CNC and robotic equipment with 24-48 hour approvals.

A major reason equipment financing pencils out so well is the tax treatment. Under IRS Section 179, businesses can often deduct the full purchase price of qualifying equipment in the year it is placed in service rather than depreciating it slowly over time, and for 2026 the deduction limit sits well above $1 million for most filers.

That write-off reduces taxable income and effectively lowers the after-tax cost of borrowing, which means a 12% headline rate can feel meaningfully cheaper once the deduction is applied.

3. Working Capital Loans and Lines of Credit

Working capital financing covers the everyday operational expenses that keep a factory running between the moment you spend on production and the moment customers pay. This category includes term loans, revolving lines of credit, and the new SBA MARC program. A revolving line is especially valuable for manufacturers because you draw only what you need, pay interest only on the balance, and replenish the line as receivables come in, which smooths out the natural cash swings of seasonal or order-driven production.

4. Commercial Real Estate Loans for Facilities

When a manufacturer needs to buy, build, or renovate a facility, a commercial real estate loan provides long-term, fixed-rate financing tied to the property. The SBA 504 program dominates here because it pairs a conventional lender with a Certified Development Company to deliver low down payments and fixed rates over long terms. Interest rates for SBA 504 loans are based on the 10-year Treasury note, are fixed for the life of the loan, and typically fall within a 5% to 7% range depending on market conditions, usually requiring a down payment of at least 10% of the project cost.

4. Invoice Factoring and Purchase Order Financing

Invoice Factoring and purchase order financing solve the receivables problem directly. Factoring lets you sell unpaid invoices to unlock cash, often within a day or two, instead of waiting out long payment terms. This approach can unlock cash tied up in unpaid receivables, usually within 24 to 48 hours of invoice generation, rather than waiting 60 to 90 days. If you want to see the mechanics in detail, our guide on how invoice factoring improves cash flow breaks down the process step by step.

Purchase order financing, meanwhile, funds large orders and seasonal production runs so you can fulfill big contracts without draining cash reserves. Both tools are about timing, not long-term debt, and they shine when a factory is growing faster than its cash flow can support.

Manufacturing Loan Options Compared at a Glance

The table below summarizes the primary financing products, what each fund does best, typical cost ranges in 2026, and the situations where each one fits. Use it as a quick reference when matching a loan to a specific need.

| Loan Type | Best For | Typical 2026 Cost | Typical Term | Funding Speed |

| SBA 7(a) | Working capital, equipment, refinancing, mixed needs | Prime + margin (often low-to-mid teens APR) | Up to 10–25 years | 2–6 weeks |

| SBA 504 | Real estate and long-life equipment | ~5%–7% fixed | 10, 20, or 25 years | 4–8 weeks |

| SBA MARC | Revolving working capital for manufacturers only | Below conventional working capital rates | Revolving line | 2–6 weeks |

| Equipment Financing | Machinery, CNC, robotics, tooling | 6%–12% APR (qualified) | 3–10 years | 24–48 hours |

| Working Capital Line | Payroll, raw materials, cash gaps | Varies; higher than SBA | Revolving | 1–7 days |

| Commercial Real Estate | Buying or building a facility | ~5%–7% fixed (504) | 20–25 years | 4–8 weeks |

| Invoice Factoring | Unlocking cash from receivables | Factor fee per invoice | Per invoice | 24–48 hours |

A clear takeaway emerges from this comparison: SBA-backed financing delivers the lowest cost but takes longer to close, while equipment financing and factoring move fast at a somewhat higher price. Smart manufacturers often combine them, using SBA money for big fixed assets and faster products to handle immediate needs.

How to Qualify for a Manufacturing Business Loan

Qualifying for manufacturing financing comes down to three core factors that nearly every lender evaluates: business experience, credit, and cash flow. While banks do not have universal rules about what makes a business creditworthy, most will evaluate three key factors: experience, credit and cash flow. Strengthening each one before you apply materially improves both your approval odds and your rate.

Time in business and revenue history carry heavy weight. Most institutional and SBA lenders want to see an established operation rather than a pre-revenue startup. The ideal manufacturing borrower for institutional and SBA lenders typically has $1M or more in annual revenue with 12 or more months of operating history, while startups and pre-revenue manufacturers are usually not yet the right fit for SBA and institutional lenders. If you are earlier in your journey, equipment financing tied to a specific asset is often more accessible than a general SBA term loan.

Credit profile matters for both approval and pricing. Borrowers with good to excellent credit, generally a score of 640 or higher, qualify for the most competitive equipment financing rates and may access SBA programs with even lower costs. If your score sits below that threshold, it is worth taking time to improve your business credit score before applying, since even a small increase can unlock better rates and terms.

Beyond the score, lenders examine your debt service coverage ratio to confirm your cash flow can cover the new payment with room to spare, along with the collateral value of the equipment or property being financed. For SBA loans specifically, the business must operate for profit, be physically located in the United States, and demonstrate sound enough credit to assure repayment.

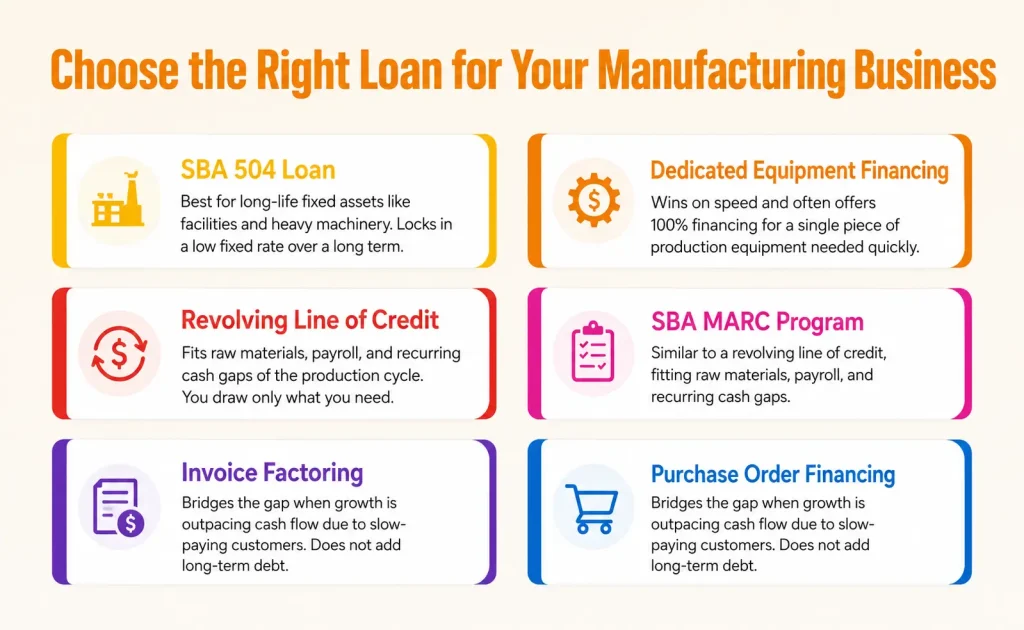

How to Choose the Right Loan for Your Manufacturing Business

Choosing the right manufacturing loan depends on what you are funding and how fast you need the capital. The decision becomes straightforward once you match the financing structure to the underlying need rather than chasing the lowest advertised rate.

For long-life fixed assets such as a facility or heavy machinery expected to last a decade or more, the SBA 504 loan is almost always the best choice because it locks in a low fixed rate over a long term. For a single piece of production equipment you need quickly, dedicated equipment financing wins on speed and often offers 100% financing.

For raw materials, payroll, and the recurring cash gaps of the production cycle, a revolving line or the new SBA MARC program fits best because you draw only what you need. And when growth is outpacing your cash flow because customers pay slowly, invoice factoring or purchase order financing bridges the gap without adding long-term debt.

The most sophisticated manufacturers do not pick just one. They stack products intentionally, for example using a 504 loan to buy a building and machinery while running a MARC line for working capital on top of it. The SBA designed MARC and 504 to complement each other: a manufacturer could use a 504 loan to buy a new facility and machinery, then use a MARC line of credit to purchase raw materials and expand inventory. Layering this way keeps your cost of capital low on big assets while preserving flexibility for day-to-day operations.

Common Mistakes Manufacturers Make When Borrowing

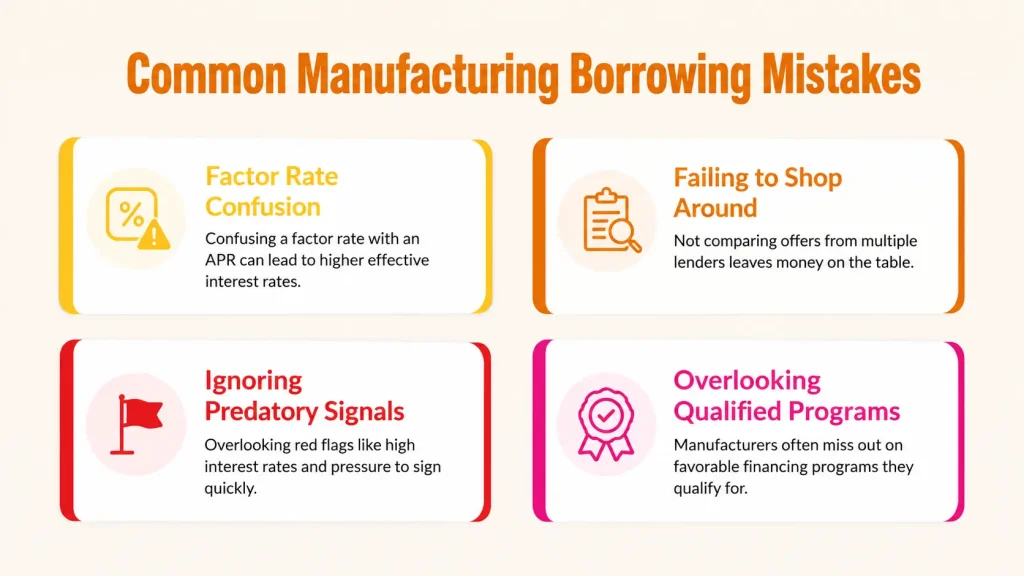

The most expensive borrowing mistakes are usually avoidable. The first is confusing a factor rate with an APR. Many online lenders use a factor rate expressed as a decimal like 1.20, which means a $50,000 advance is repaid as $60,000, and in the short term the effective APR can be far higher than 20%. Always convert a factor rate to an APR before comparing offers, and treat any lender who refuses to do so as a warning sign. These pricing traps are part of a wider set of common term loan mistakes to avoid quietly draining small business profits.

A second mistake is failing to shop with multiple lenders, which leaves real money on the table. The spread between the best and worst rate on the same machine can be nearly $27,000 over the life of a loan, which is exactly why shopping multiple lenders and improving your credit profile pays off. A third mistake is ignoring predatory loan signals.

The SBA itself warns borrowers to watch out for specific red flags. Warning signs include interest rates significantly higher than competitors, fees that exceed 5% of the loan value, pressure to sign quickly, requests to leave signature boxes blank, and a lender failing to disclose the annual percentage rate and full payment schedule.

Finally, many manufacturers overlook programs they actually qualify for. Rural facilities frequently miss out on favorable financing. If a manufacturing facility is located in a rural area with a population under 50,000, it may qualify for USDA Business and Industry loans, one of the most underutilized programs in manufacturing finance, and most areas outside major metro centers qualify as rural under USDA definitions.

Why 2026 is an Exceptional Time to Finance a Manufacturing Business

The combination of policy support and competitive lending has created unusually favorable conditions for factory owners this year. Combined with the FY2026 fee waivers on loans under $1M and expanded 504 limits for manufacturers, this is the strongest SBA environment for manufacturing in a decade.

Federal policy is actively channeling capital toward domestic production. New federal policy focused on reshoring, infrastructure investment and supply chain resilience is creating strong conditions for reinvestment, with expanded SBA loan programs making this vision possible.

The practical effect for a factory owner is lower fees, higher borrowing limits, faster approvals, and a brand-new revolving credit program built specifically for your industry. The manufacturers who plan ahead and act while these incentives are live will be best positioned to expand, modernize equipment, and strengthen their operations before the fee waivers expire at the end of September 2026.

Ready to Fund Your Factory? Partner With Committed to Capital

The financing environment for manufacturers may be the best it has been in years, but capturing those advantages still requires structuring the right deal with the right lender at the right time. Committed to Capital helps factory owners cut through the complexity, compare SBA programs, equipment financing, working capital, and invoice-based options, and assemble a financing package that matches how your production actually runs.

Whether you are buying your first CNC machine, expanding into a larger facility, or simply smoothing out cash flow between orders, the team can help you move fast and borrow smart. Connect with Committed to Capital today to explore what your manufacturing business qualifies for.

Conclusion

Manufacturing business loans are not a single product but a toolkit, and the factory owners who win are the ones who match each tool to the right job. Equipment financing fuels the production floor, SBA 504 loans anchor your facility and heavy machinery, the new MARC program and working capital lines keep raw materials and payroll flowing, and invoice factoring unlocks cash trapped in slow-paying receivables. In 2026, with the SBA waiving most fees, doubling loan caps, and launching the first manufacturer-only credit program, the cost of building and growing a factory has dropped meaningfully.

The competitive advantage comes from preparation and structure rather than luck. Know your numbers, strengthen your credit and cash flow, shop multiple lenders, convert every factor rate into a true APR, and never sign under pressure. Do that, and you turn financing from a constraint into an engine for growth. Quality decisions, not just available capital, separate the manufacturers who scale from the ones who stall.