When your business needs new machinery, vehicles, or technology, you face an early and important decision: should you finance the equipment and work toward ownership, or lease it and pay only for the time you use it? The choice between equipment financing vs. leasing affects your upfront cash, your monthly payments, your tax position, and how much you spend over the full life of the asset.

There is no single answer that fits every business. The cheaper option depends on how long you plan to use the equipment, how quickly it loses value, and how much cash you want to keep available. This guide breaks down how each option works, compares them side by side on real cost factors, and gives you a clear framework to decide which one actually saves you more money.

Equipment Financing vs. Leasing: The Quick Answer

Equipment Financing usually saves more money over the long term when you plan to keep the equipment well beyond the loan term, because you eventually own an asset you no longer pay for. Leasing usually saves more on upfront cost and works better for equipment that becomes outdated quickly or that you only need for a short period. In short, financing rewards long-term use and ownership, while leasing rewards flexibility and lower initial spending.

How Committed to Capital Helps You Choose

Choosing between financing and leasing is easier when someone helps you compare the real numbers instead of guessing. Committed to Capital works with business owners to match the right equipment acquisition strategy to their goals, cash flow, and growth plans. Whether you run a construction company, a manufacturing facility, a medical practice, or a service business, the team can walk you through financing and leasing options so you understand the full cost of each before you commit.

If you want a deeper look at the available routes, the guide on equipment financing options for small business is a helpful starting point.

What is Equipment Financing?

Equipment financing is a business loan used to purchase the equipment your company needs to operate or grow. You typically make a down payment, then repay the remaining balance plus interest over a fixed term. The equipment itself usually serves as collateral, which often makes approval more accessible than an unsecured loan.

When the loan term ends, you own the equipment outright. That ownership is the defining feature of financing. It suits businesses that expect to use the same equipment for many years and want to build long-term value rather than pay indefinitely for access.

Manufacturers and contractors often choose this route, as covered in the manufacturing business loans guide and the complete guide to construction business loans, where durable, long-life equipment is central to operations.

What is Equipment Leasing?

Equipment leasing lets you pay regular payments to use equipment without buying it. Leases usually require little or no down payment, which keeps more cash in your business at the start. At the end of the lease term, you typically choose to return the equipment, renew the lease, or purchase it at a set price.

Leasing appeals to businesses that value flexibility and predictable payments, especially when equipment becomes obsolete quickly. The two most common lease structures behave very differently, so it helps to understand both before signing.

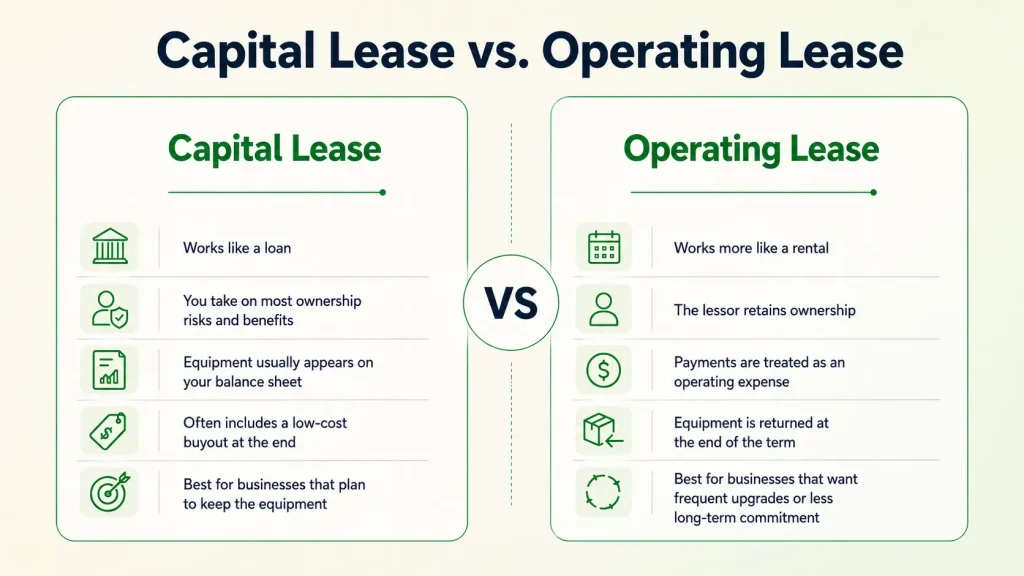

Capital Lease vs. Operating Lease

A capital lease functions much like a loan. You take on most of the ownership risks and benefits, the equipment usually appears on your balance sheet, and you often have the option to buy it for a small amount at the end. It fits businesses that intend to keep the equipment.

An operating lease is closer to a rental. The lessor retains ownership, payments are treated as an operating expense, and you return the equipment when the term ends. It fits businesses that want to upgrade frequently or avoid being tied to aging equipment.

Equipment Financing vs. Leasing: Side-by-Side Cost Comparison

The smartest comparison looks past the monthly payment and weighs the full cost of each option. The table below shows how financing and leasing differ across the factors that matter most to your budget.

| Cost Factor | Equipment Financing | Equipment Leasing |

| Upfront cost | Usually requires a down payment | Little to no money down |

| Monthly payment | Higher, but ends when the loan is paid off | Often lower, but continues for the lease term |

| Total cost over equipment’s life | Lower for long-term use; payments stop | Can be higher if you keep paying year after year |

| Ownership | You own the asset outright at the end | You return, renew, or buy at the end |

| Resale value | Yours to sell once the loan is repaid | None, unless you exercise a purchase option |

| Obsolescence risk | You carry the risk of outdated equipment | Risk shifts mostly to the lessor; easier to upgrade |

| Maintenance responsibility | Falls on you as the owner | Often shared with or covered by the lessor |

| Tax treatment | Deduct depreciation and loan interest | Deduct full lease payments as an expense |

| Best for | Durable equipment used for many years | Fast-aging tech or short-term needs |

Consider a $50,000 machine. If you finance it and use it for seven years, your payments end after the loan term and you operate the remaining years with no equipment cost, then potentially sell it. If you lease that same machine but only need it for two years, leasing likely costs less overall and spares you from owning a depreciating asset you no longer use. The right answer hinges on your time horizon.

Which Option Actually Saves More Money?

“Saves more” depends on total cost of ownership, not the size of a single payment. A lower monthly lease payment can feel cheaper while quietly costing more over many years of continuous use. Financing carries higher monthly costs but ends, leaving you with a paid-off asset.

For durable equipment you will use for the long haul, such as heavy machinery or commercial vehicles, financing typically saves more money because ownership eliminates future payments and may return resale value. For equipment that ages fast or that you need only temporarily, leasing typically saves more by lowering upfront cost and removing the burden of obsolescence. Match the option to how long the equipment stays valuable and useful to your business.

Tax Implications of Financing vs. Leasing

Both options can offer tax advantages, but they work differently. With financed equipment, you may be able to deduct depreciation and the interest portion of your payments, since you own the asset. With leasing, you can often deduct the full lease payment as a business operating expense, which can simplify your accounting.

Section 179 of the tax code allows many businesses to deduct the cost of qualifying equipment, and it can apply to both financed and certain leased equipment. Because deduction limits and eligibility rules change, confirm the current figures on the IRS and review your specific situation with a qualified tax professional before deciding based on tax treatment alone.

When to Finance and When to Lease

The best choice comes down to your usage timeline, cash position, and appetite for ownership. The criteria below make the decision clearer.

When Equipment Financing Makes More Sense

- You plan to use the equipment for many years, well past the loan term.

- The equipment holds its value and resists obsolescence.

- You want to own the asset and build long-term business value.

- You can comfortably manage a down payment and higher monthly payments.

When Leasing Makes More Sense

- The equipment is technology that becomes outdated quickly.

- You only need the equipment for a short or seasonal period.

- Preserving cash flow is a current priority for your business.

- You prefer predictable payments and the ability to upgrade regularly.

How to Choose the Right Equipment Acquisition Strategy

Start by estimating how long the equipment will stay useful and valuable to your operation. Next, calculate the total cost of financing versus leasing across that full period, not just the monthly difference. Then factor in your cash flow needs, your tax situation, and whether ownership benefits your long-term plans. Finally, compare real offers so the decision rests on actual terms rather than assumptions.

Your broader funding picture matters too. Strong financials open better terms, which is why the steps in how to improve your business credit score before applying for capital are worth reviewing first. If cash flow timing is the real obstacle, options like revenue-based financing or invoice factoring to improve cash flow may pair well with an equipment decision.

It also helps to understand how the wider lending environment, including how inflation and interest rates affect small business loans, shapes the rates you are offered.

Compare Your Equipment Financing and Leasing Options

You do not have to make this decision alone or based on guesswork. The right comparison weighs your equipment timeline, cash flow, and tax position against real terms, and that is exactly where guidance pays off.

To get options tailored to your business, request a consultation with Committed to Capital and review your choices side by side. You can also explore the dedicated equipment financing page to see how funding can be structured around the specific asset you need.

Final Thoughts

The equipment financing vs. leasing decision rarely comes down to a single number. Financing tends to save more money over the life of equipment you will keep and use for years, because ownership ends your payments and may return resale value. Leasing tends to save more on upfront cost and suits equipment that becomes outdated quickly or that you need only for a short time.

Before you commit, run a full total-cost comparison for both options across the period you actually expect to use the equipment, and weigh your cash flow and tax situation alongside the raw numbers. A clear, side-by-side look is the most reliable way to choose the option that protects both your budget and your growth.