Growth rarely waits for your bank balance to catch up. A new contract, a seasonal rush, or a marketing opportunity often shows up before the cash to fund it does. Revenue-based financing solves that timing gap by giving you capital now and tying repayment directly to what you earn each month. Instead of a fixed payment that ignores how business is actually going, you pay more when sales are strong and less when they slow down.

Key Takeaways:

- Revenue-based financing gives your business upfront capital that you repay as a percentage of monthly revenue, so payments rise and fall with your actual sales.

- Unlike a traditional term loan, revenue-based financing does not require equity, and approval leans more on consistent revenue than on your personal credit score.

- This funding model fits subscription, ecommerce, seasonal, and service businesses that have steady income but uneven month-to-month cash flow.

- The biggest advantages are flexible repayment, fast access to capital, and low documentation, while the main tradeoff is a higher effective cost than a bank loan.

- Comparing revenue-based financing against a line of credit or invoice factoring helps you match the funding structure to your specific cash flow problem.

- Qualifying is usually straightforward: businesses with strong monthly revenue, a business bank account, and clean deposit history are strong candidates.

This guide explains what revenue-based financing is, how it works, who it suits, and how it compares to other funding options. You will also see what it takes to qualify and how to decide whether it is the right fit for your business.

What is Revenue-Based Financing?

Revenue-based financing is a funding method where a business receives a lump sum of capital and repays it through a fixed percentage of its ongoing revenue until a set total amount is paid back. The repayment amount is not fixed from month to month. It moves with your sales, which is why this option appeals to companies with variable or seasonal income.

The lender is not buying a share of your company, and you are not committing to a rigid monthly installment. You agree to repay the advance plus a fee, and the pace of repayment adjusts to your performance. Strong months clear the balance faster. Slow months ease the pressure because you pay proportionally less. This structure keeps repayment aligned with the money actually coming through the door.

How Revenue-Based Financing Differs From a Traditional Loan

A traditional term loan gives you a set amount at a fixed interest rate with the same payment due every month, regardless of how your business is performing. That predictability works well for stable, established companies but can strain a business with uneven revenue.

Revenue-based financing flips that structure. There is no fixed monthly payment and usually no equity given up. Approval depends heavily on your revenue history rather than a high credit score, and funding often arrives in days rather than weeks. The tradeoff is cost: because the model carries more flexibility and risk for the funder, the total repayment is typically higher than a comparable bank loan.

How Does Revenue-Based Financing Work?

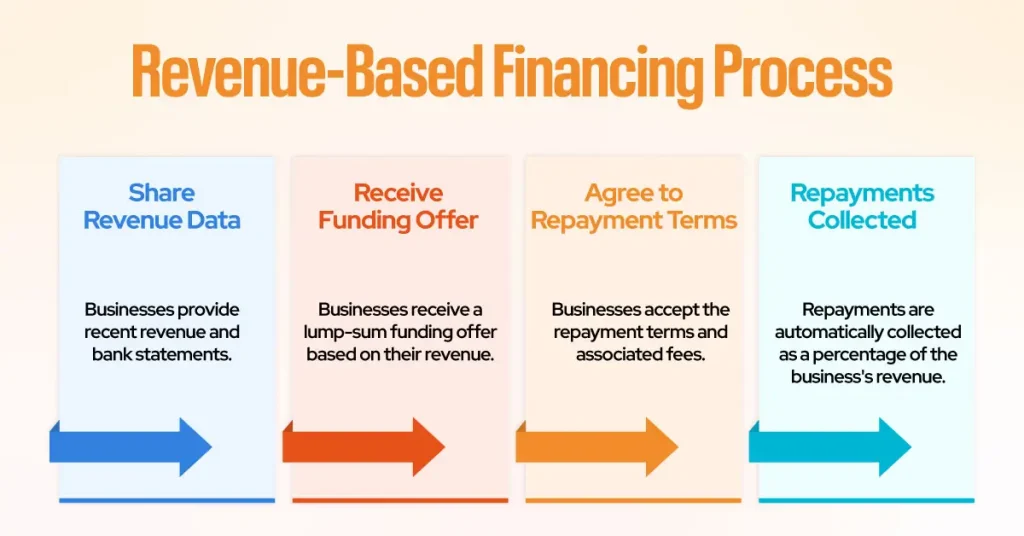

The process is built around your revenue data. Instead of digging through years of tax returns and collateral schedules, a funder looks at how much money your business brings in and how consistently. From there, the mechanics are straightforward.

- You share recent revenue and bank statements so the funder can verify consistent income.

- You receive a funding offer, usually a lump sum, based on your average monthly revenue.

- You agree to repay a set total, the advance plus a fixed fee, often expressed as a factor rate.

- Repayments are collected as an agreed percentage of your revenue until the total is repaid.

Because repayment is a percentage of sales rather than a flat figure, the dollar amount you send changes with your performance. That is the core benefit and the reason this option suits businesses whose income is not the same every month.

A Simple Repayment Example

Say a business receives $50,000 and agrees to repay $60,000 total, with 10% of monthly revenue going toward repayment. In a $100,000 revenue month, the business repays $10,000. In a slower $60,000 month, it repays $6,000. The percentage stays the same, but the payment shrinks when sales dip, protecting cash flow during quiet stretches. The business keeps paying at that rate until the agreed $60,000 total is cleared.

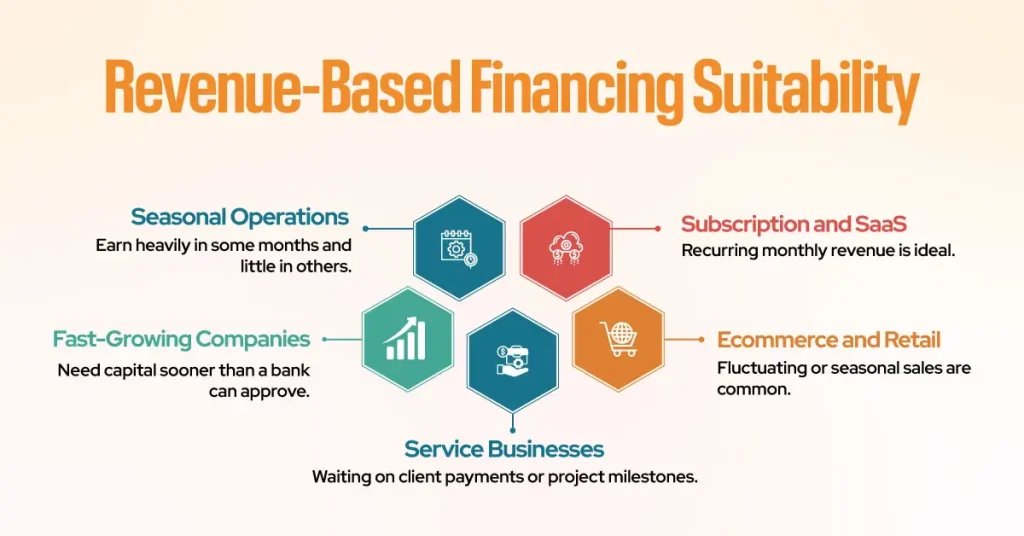

Who is Revenue-Based Financing Best For?

Revenue-based financing is best for businesses that generate steady revenue but experience uneven cash flow across the month or year. If your income is real and recurring but arrives on an unpredictable schedule, this model tends to fit better than a fixed-payment loan.

It is especially useful for the following types of businesses:

- Subscription and SaaS companies with recurring monthly revenue.

- Ecommerce and retail businesses with fluctuating or seasonal sales.

- Service businesses waiting on client payments or project milestones.

- Fast-growing companies that need capital sooner than a bank can approve it.

- Seasonal operations that earn heavily in some months and little in others.

For a closer look at how this plays out in one regional market, our guide on Revenue-Based Financing: What It Is and How It Works in Pennsylvania walks through real local scenarios in more detail.

Key Benefits of Revenue-Based Financing

The appeal of revenue-based financing comes down to flexibility and speed. For the right business, it removes several of the pain points that make traditional lending frustrating, from rigid monthly payments to long approval timelines and heavy paperwork. Instead of forcing your business to fit a lender’s fixed formula, this model shapes itself around how your business actually earns.

The core advantages are easy to see when you line them up:

- Payments that flex with sales. You pay more in strong months and less in slow ones, which protects cash flow when you need it most. This is the single biggest reason seasonal and cyclical businesses favor the model, because repayment never demands more than your revenue can comfortably support.

- No equity given up. You keep full ownership and control of your business, unlike raising money from investors. There is no board seat to hand over and no share of future profits to surrender, so the value you build stays yours.

- Faster access to capital. Approval and funding are often measured in days because the review centers on revenue rather than collateral. That speed lets you act on a time-sensitive opportunity, such as a bulk inventory deal or a marketing window, before it disappears.

- Lower documentation. Expect fewer forms and less collateral paperwork than a conventional bank loan. For busy owners without a full finance team, that lighter lift can be the difference between applying and giving up.

- Credit-flexible approval. Funding decisions lean on revenue performance rather than a high credit score, which opens the door for newer businesses or owners still rebuilding credit.

Taken together, these benefits make revenue-based financing a practical bridge for businesses that are healthy and growing but do not fit the rigid box a traditional lender expects. It is not about replacing every other funding tool. It is about giving strong, revenue-generating companies a faster, more forgiving way to fund their next step without sacrificing ownership or stalling on paperwork.

Potential Drawbacks and What to Watch For

No funding option is right for every situation, and revenue-based financing has real tradeoffs. Understanding them upfront helps you decide with clear eyes rather than being surprised later. The table below breaks down each drawback, what it means for your business, and who tends to feel it most.

| Drawback | What It Means for Your Business | Who It Affects Most |

| Higher effective cost | The convenience and flexibility usually come at a higher total cost than a bank loan or SBA loan. You are paying a premium for speed, flexible repayment, and easier approval. | Businesses that could qualify for low-rate bank or SBA financing and have time to wait for it. |

| Revenue dependency | Because repayment is tied to sales, a strong month means a larger payment. Growth is good, but it also accelerates how much you repay in your busiest periods. | Fast-scaling companies with sharp revenue spikes month to month. |

| Not ideal for very thin margins | Dedicating a fixed percentage of revenue to repayment can strain day-to-day operations when there is little profit cushion to absorb it. | Low-margin businesses such as high-volume retail or price-competitive services. |

| Shorter repayment windows | These arrangements are usually built for near-term needs, so they rarely stretch over the multi-year horizon a large purchase may require. | Owners funding long-term projects like real estate, major expansion, or heavy equipment. |

| Frequent payment collection | Repayments are often drawn on a daily or weekly basis rather than monthly, which requires steady cash flow discipline. | Businesses with irregular deposit timing or limited cash reserves between sales cycles. |

| Not a fix for underlying problems | Revenue-based financing smooths timing gaps, but it will not solve a business model that is unprofitable or losing customers. | Companies using financing to cover ongoing losses rather than fund genuine growth. |

The takeaway is simple: revenue-based financing rewards businesses with healthy, consistent sales that need speed and flexibility, and it costs more for that convenience. If long-term, low-cost capital is your priority and you can meet stricter approval standards, a conventional loan or line of credit may serve you better. Weigh these tradeoffs against the benefits before you decide, and match the funding structure to the problem you are actually trying to solve.

If long-term, low-cost capital is your priority and you have the credit and time to qualify, a conventional loan may serve you better. Some owners in that position explore whether to restructure existing debt instead; our article on Can New York Small Businesses Refinance High-Cost Loans? Pros & Cons is a useful starting point for that decision.

Revenue-Based Financing vs. Other Funding Options

Choosing the right funding tool depends on the problem you are solving. Revenue-based financing shines when cash flow is uneven, but two other common options solve related problems in different ways.

Revenue-Based Financing vs. a Business Line of Credit

A business line of credit and revenue-based financing both give you fast access to working capital, but they solve different problems. A line of credit gives you a revolving limit you can draw from, repay, and reuse as needed, which makes it well suited to ongoing or unpredictable expenses. Revenue-based financing delivers a single lump sum upfront with repayment tied to a percentage of your sales, which makes it a better match for a specific growth push or a clearly defined need.

The clearest way to see the difference is to compare them side by side:

- Funding structure. A line of credit is revolving and reusable, while revenue-based financing is a one-time lump sum.

- Repayment. A line of credit follows a set schedule on the amount you draw, whereas revenue-based financing flexes with your monthly revenue.

- Cost. A line of credit often costs less over time, while revenue-based financing usually carries a higher effective cost in exchange for flexibility.

- Approval requirements. A line of credit typically demands stronger credit and more documentation, while revenue-based financing leans on revenue history rather than your credit score.

- Speed. Revenue-based financing is often funded within days, while a line of credit can take longer to approve and set up.

So which one fits your situation? Choose a line of credit if you want a reusable safety net for recurring or uncertain costs and you can meet the stricter approval standards. Choose revenue-based financing if you need capital quickly, prefer payments that adjust to your sales, or do not yet qualify for a conventional line of credit.

Many growing businesses eventually use both, tapping revenue-based financing for a near-term opportunity while building the credit profile a line of credit rewards. If you want to understand the approval side, our guide on How to Qualify for a Business Line of Credit breaks down exactly what lenders look for.

Revenue-Based Financing vs. Invoice Factoring

Revenue-based financing and invoice factoring both unlock cash without a traditional loan, but they pull from different sources. Invoice factoring turns your unpaid invoices into immediate cash by selling those receivables to a factor at a discount, so it fits businesses stuck waiting on slow client payments. Revenue-based financing does not depend on outstanding invoices at all; it draws on your overall revenue instead, which makes it a better fit when your income comes from many smaller sales rather than a handful of large invoices.

Here is how the two compare at a glance:

- What it draws on. Factoring is tied to specific unpaid invoices, while revenue-based financing is based on your total monthly revenue.

- Best-fit business. Factoring suits B2B companies that invoice clients on net terms, whereas revenue-based financing suits ecommerce, subscription, and retail businesses with steady sales.

- Customer involvement. With factoring, the factor may contact your customers to collect on invoices, while revenue-based financing keeps repayment between you and the funder.

- Cash flow trigger. Factoring solves the problem of waiting weeks for invoices to clear, while revenue-based financing solves the broader problem of uneven month-to-month income.

- Repayment feel. Factoring is settled as your customers pay their invoices, while revenue-based financing is repaid as a percentage of your ongoing sales.

The right choice comes down to where your cash flow actually gets stuck. If slow-paying customers are your core issue and most of your revenue sits in unpaid invoices, factoring is often the cleaner, more direct fix. If your income is spread across everyday sales and the real challenge is uneven timing rather than late invoices, revenue-based financing usually fits better.

Some businesses even use them together, factoring large invoices while relying on revenue-based financing to smooth out general cash flow. To see how factoring works in a real regional market, read our overview of How Invoice Factoring Improves Small Businesses Cash Flow in Philadelphia, PA.

Talk to Committed to Capital About Flexible Funding

Every business has a different cash flow story, and the best funding choice depends on yours. The team at Committed to Capital helps business owners compare options and structure revenue-based financing around real revenue rather than a rigid formula. Based in Pitman, New Jersey, and serving businesses nationwide, the team focuses on clear terms and honest guidance.

If you want to see what flexible repayment could look like for your business, reach out to Committed to Capital to talk through your goals and get a straightforward assessment of your options.

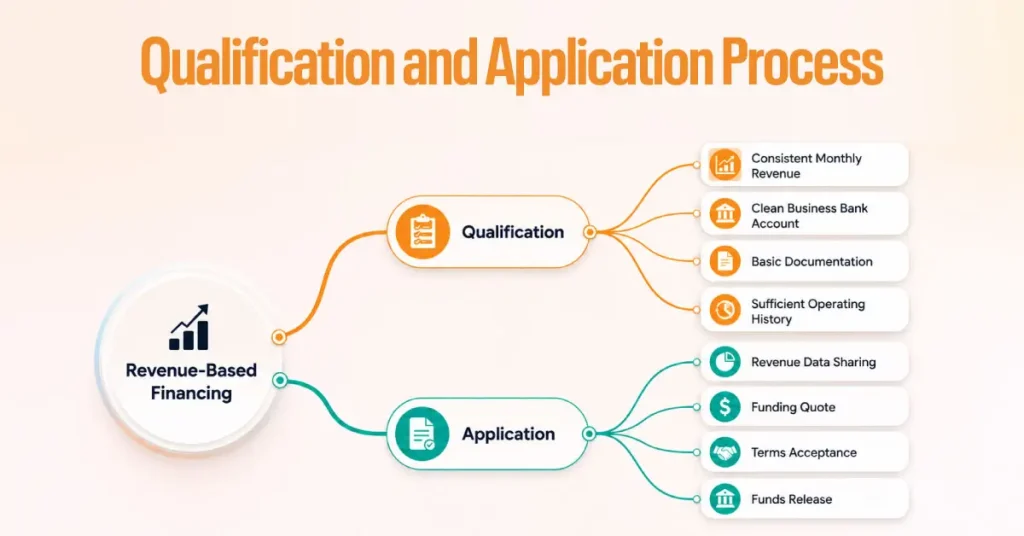

How to Qualify and Apply for Revenue-Based Financing

Qualifying for revenue-based financing is usually simpler than qualifying for a traditional loan because the focus is on your revenue, not your credit score or collateral. Most funders look for a few core things.

- Consistent monthly revenue that demonstrates your business can support repayment.

- A business bank account with a clean, verifiable deposit history.

- Basic documentation such as a valid ID and recent bank statements.

- Enough operating history to show reliable, recurring income.

The application itself is typically quick. You share your revenue data, receive a funding quote based on performance, and, once you accept the terms, funds are often released within days. Because there is no heavy collateral review, the timeline is far shorter than a conventional loan. To review current requirements and see what your business could qualify for, visit the revenue-based financing service page.

Get Started With Committed to Capital

If uneven cash flow is holding back your next move, revenue-based financing may be the flexible bridge you need. The right partner makes the difference between a confusing process and a clear one. Committed to Capital works with business owners to match funding to their actual revenue and growth plans, with practical guidance and no pressure.

Ready to explore your options? Contact the Committed to Capital team to request a consultation and find the funding structure that fits your business.

Final Thoughts

Revenue-based financing is a flexible way to access capital when your income is strong but uneven. By tying repayment to a percentage of revenue, it eases pressure during slow months and moves faster than traditional lending, without asking you to give up equity. The tradeoff is a higher effective cost, so it fits best when speed and flexibility matter more than securing the lowest possible rate.

The smartest approach is to match the funding tool to the problem you are actually solving. Compare revenue-based financing against a line of credit and invoice factoring, weigh the benefits against the drawbacks, and choose the structure that supports your cash flow rather than fighting it. When you are ready to move, a knowledgeable funding partner can help you turn that decision into capital.