For small and medium-sized businesses, 2026 is not a year for guesswork. Costs remain elevated, technology is changing how companies operate, and business owners are under pressure to move faster while protecting margins.

Key Takeaways

- Business loans can help fund growth, support cash flow, and keep operations stable.

- The right loan depends on your business goal, timeline, credit profile, and funding urgency.

- SBA loans usually offer strong rates and longer terms, but approval often takes more time and documentation.

- Revenue-based financing and merchant cash advances can provide fast funding, but they typically cost more.

- Business lines of credit offer flexibility for managing short-term and day-to-day cash flow needs.

- Preparing documents like bank statements, tax returns, and revenue records can improve approval speed and loan readiness.

- Working with the right lending partner can make it easier to match your business with a suitable funding option.

In this environment, access to capital is more than a convenience. It is often the difference between staying reactive and building a business that can grow with confidence. Business loans remain one of the most practical tools for funding operations, managing cash flow, investing in equipment, and pursuing expansion at the right time.

Whether you run a restaurant, ecommerce brand, service company, franchise, startup, or manufacturing business, the financing decision you make today can shape your next several years.

The right loan can give you room to hire, buy inventory, upgrade technology, stabilize working capital, or open a new location. The wrong loan can drain cash flow, create repayment pressure, and limit future flexibility. That is why choosing funding strategically matters more than ever.

Why Business Loans Matter in 2026

Business owners are operating in a more demanding lending environment than they did before the pandemic era. Lenders still want to extend capital, but they are paying closer attention to cash flow, financial reporting, repayment ability, and risk by industry.

At the same time, many companies need money for more than survival. They need it to compete. That includes investing in automation, software, marketing, staff, equipment, inventory, and customer experience.

This is why business loans continue to matter. Financing gives owners the ability to act when opportunities appear instead of waiting until momentum is gone. It can help bridge timing gaps between receivables and payables, absorb temporary slowdowns, or fund a move that increases long-term revenue. Used well, capital is not just debt. It is leverage for better business decisions.

Why Business Loans Are Essential for SMBs

Business loans serve as the lifeblood of growth and stability. Without financing, many owners struggle to pay employees, buy inventory, invest in marketing, or expand operations.

In 2026, the importance of loans is even more visible. Companies need financing to compete in digital markets, adopt automation tools, and manage increasing supply chain costs. Having the right loan in place allows you to stabilize operations while preparing for long term success.

With Committed to Capital by your side, getting the funding you need to grow, compete, and succeed in 2026 has never been easier.

What Has Changed in Business Lending

The lending market in 2026 is broader than many owners realize. Traditional banks still play an important role, especially for established businesses with strong financials and collateral.

But they are no longer the only serious path. Fintech lenders, specialty finance companies, community-based lenders, and SBA-backed options have made the market more competitive and more segmented. Different lenders now serve different borrower profiles, funding timelines, and risk levels.

That creates more opportunity, but it also creates more complexity. A fast approval does not always mean a good deal. A lower advertised rate does not always reflect the full borrowing cost. Some products are built for long-term investments, while others are better suited to short-term gaps. Business owners who understand these differences are much more likely to choose financing that supports growth instead of creating new pressure.

How to Choose the Right Loan in 2026

Before comparing lenders, define the purpose of the loan. Are you covering payroll during a slow stretch? Buying equipment with a long useful life? Opening a second location?

Refinancing expensive debt? Purchasing commercial real estate? Your use case should guide the structure of the loan. Matching the wrong product to the wrong need is one of the most common financing mistakes.

Next, think about timing. If you need capital in days, a traditional bank process may not fit. If you can wait several weeks and your business qualifies, a lower-cost product may save significant money over time. Then evaluate the total cost, not just the rate.

Look at origination fees, underwriting fees, factor rates, repayment frequency, collateral requirements, personal guarantees, and any prepayment penalties. A loan that looks attractive on the surface can become expensive once the full structure is clear.

Finally, look at repayment in the context of real cash flow. A weekly or daily repayment structure may feel manageable during strong sales periods, but it can become stressful when revenue softens. The best loan is not simply the one you can get approved for. It is the one your business can comfortably use and repay while still protecting operational flexibility.

Secure the right loan now contact Committed to Capital for expert advice, faster approvals, and customized funding solutions for your small business.

Comparison Table of Business Loan Options in 2026

| Loan Type | Typical Amount | Term Length | Funding Speed | Best For |

| SBA 7a Loan | 250k to 5M | Up to 25 years | 4 to 8 weeks | Acquisitions, expansion |

| SBA 504 Loan | 500k to 5M | 10 to 25 years | 6 to 10 weeks | Real estate or equipment purchase |

| SBA Express Loan | Up to 500k | Up to 10 years | 2 to 3 weeks | Smaller projects |

| SBA Microloan | Up to 50k | Up to 6 years | 2 to 6 weeks | Startups and microbusinesses |

| Bank Term Loan | 100k to 5M | 3 to 10 years | 4 to 6 weeks | Established SMBs |

| Business Line of Credit | 50k to 500k | Revolving | 1 to 3 weeks | Cash flow management |

| Equipment Financing | 50k to 1M | 3 to 7 years | 1 to 3 weeks | Buying or leasing equipment |

| Invoice Financing | 10k to 1M | 1 to 6 months | 3 to 7 days | B2B companies |

| Merchant Cash Advance | 5k to 500k | 3 to 12 months | 1 to 3 days | Quick funding |

| Revenue Based Financing | 50k to 2M | Until paid off | 1 to 2 weeks | SaaS and ecommerce |

| Asset Based Lending | 100k to 5M | 1 to 5 years | 3 to 5 weeks | Growth financing |

| Commercial Real Estate Loan | 500k to 10M | 10 to 25 years | 5 to 8 weeks | Buying property |

| Purchase Order Financing | 50k to 2M | Until paid | 2 to 3 weeks | Large order fulfillment |

| Startup Loan | Up to 250k | 1 to 5 years | 3 to 5 weeks | New businesses |

| Franchise Financing | 50k to 500k | 3 to 10 years | 2 to 4 weeks | Franchise startups |

| Export Working Capital | 100k to 2M | Up to 3 years | 3 to 6 weeks | Exporters |

Expanded Types of Loans

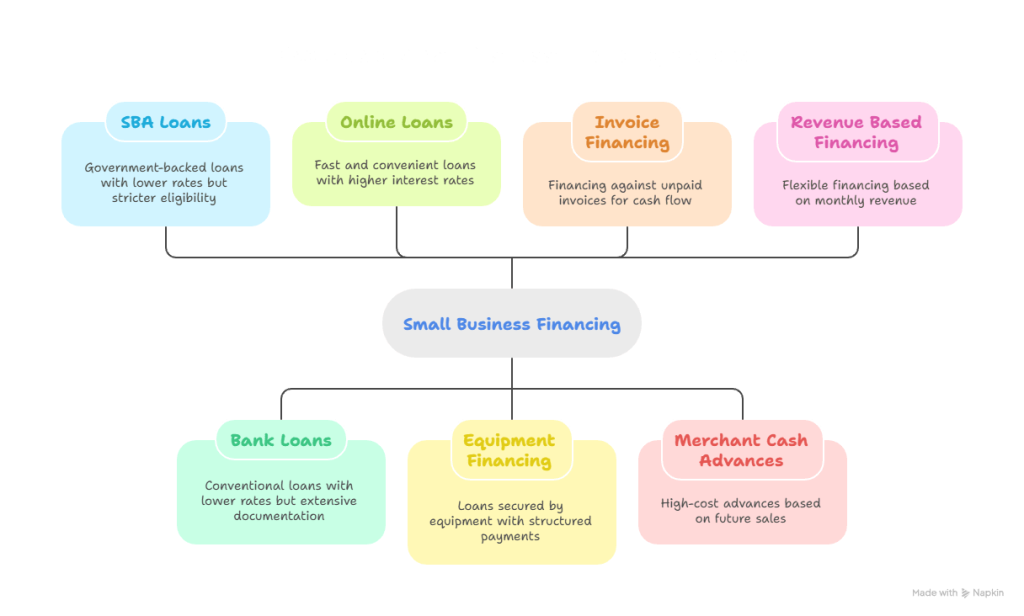

SBA Loans

The Small Business Administration continues to support American entrepreneurs through the 7a, 504, Express, and Microloan programs. These loans provide lower rates and longer repayment terms because they are partially guaranteed by the government. The tradeoff is stricter eligibility and longer approval timelines.

SBA loans remain one of the strongest options for qualified borrowers because they are partially guaranteed by the government and often come with favorable terms. The most recognized programs on the page are SBA 7(a), SBA 504, Express, and Microloans.

These options can work well for expansion, acquisitions, equipment, real estate, and other strategic needs. The tradeoff is that approval can take longer and documentation tends to be heavier.

Bank Loans and Credit Unions

Conventional loans remain the best choice for established businesses with solid revenue and strong credit. Banks provide term loans and lines of credit at lower rates compared to alternative lenders but require extensive documentation and often collateral.

Conventional bank financing is often best for established businesses with strong revenue, clean books, and solid credit. These loans may offer lower costs than alternative products, but qualification standards are typically stricter. Banks may require collateral, detailed financial statements, and a stronger operating history than online lenders.

Business Lines of Credit

Business line of credit is one of the most flexible funding tools available. Instead of receiving one lump sum, you draw what you need up to an approved limit. That makes this option useful for payroll gaps, inventory purchases, uneven receivables, and recurring working-capital needs. For many owners, a line of credit is not just financing. It is a financial buffer that helps smooth operations.

Online and Fintech Loans

Online lenders offer speed and convenience. Applications are streamlined, funding is fast, and requirements are flexible. However, interest rates are usually higher. These loans are suitable for businesses that need quick access to cash or cannot qualify for bank financing.

Equipment Financing

If you are purchasing machinery, vehicles, medical devices, kitchen systems, or other operational equipment, equipment financing can be a strong fit. Because the equipment often serves as collateral, approval may be easier than with an unsecured product. This financing also aligns well with assets that produce value over several years, making repayment more practical.

This option is ideal when purchasing machinery, vehicles, or technology. The equipment itself acts as collateral which makes approval easier. Payments are structured to match the useful life of the asset.

Invoice Financing and Factoring

For B2B companies that wait on customer payments, invoice financing and factoring can unlock cash tied up in receivables. Invoice financing typically means borrowing against unpaid invoices, while factoring generally involves selling those invoices to a third party.

These products can improve short-term liquidity, especially for companies with solid receivables but uneven cash timing. They can also cost more than owners expect, so fee structure matters.

If your business invoices other companies, these tools allow you to unlock cash tied up in receivables. Financing lets you borrow against unpaid invoices, while factoring means selling them outright. This helps maintain cash flow but can be expensive.

Merchant Cash Advances

A Merchant Cash Advance provides upfront cash in exchange for a share of future sales. It is often marketed around speed and accessibility, and for some businesses it can be one of the easiest products to qualify for. It is also commonly one of the most expensive. This option is usually better treated as a last-resort emergency tool than a long-term growth strategy.

Revenue Based Financing

Revenue based financing has become especially relevant for SaaS, ecommerce, and other businesses with recurring or digital sales. Instead of a fixed installment, repayment is tied to a percentage of monthly revenue. That can make payments feel more manageable when revenue fluctuates. Still, flexibility should not be confused with low cost. Owners should model several sales scenarios before accepting this structure.

This method is increasingly popular among SaaS and ecommerce companies. Payments are based on a fixed percentage of monthly revenue which means the repayment schedule adjusts with your income. It provides flexibility but can extend repayment if sales are weak.

Asset Based Lending

Asset based lending is secured by assets such as receivables, inventory, or other business collateral. For growing companies with meaningful assets, this can provide larger borrowing capacity than unsecured financing. It also comes with more reporting, lender oversight, and structure than many simpler loan products.

Commercial Real Estate Loans

Businesses buying, refinancing, or expanding property often turn to commercial real estate loans or certain SBA-backed real-estate-friendly options. These loans usually involve long repayment periods and property collateral. Business owners should pay close attention to loan-to-value expectations and debt service coverage requirements.

Purchase Order Financing

If your company receives a large order but lacks the funds to fulfill it, PO financing provides the capital needed. It is useful in manufacturing and wholesale sectors but comes with high costs.

Startup and Franchise Loans

Startups may rely on CDFIs, microloans, or online lenders since they often lack the history banks require. Franchise loans leverage brand strength and usually come with packages tailored to new franchisees. Startup loans give new business owners the capital they need to launch and grow when traditional banks may not approve early-stage companies.

Startups often struggle to qualify for traditional bank loans because they lack operating history. In those cases, microloans, online lenders, CDFIs, or specialized startup products may be more realistic entry points. Franchise financing can be easier to structure when lenders are comfortable with the franchise brand and business model. Even then, preparation and realistic projections still matter.

Export Working Capital

For businesses involved in international trade, this loan covers the gap between fulfilling orders and receiving overseas payments. The SBA supports some of these programs.

How Much Do Business Loans Cost?

One of the biggest mistakes business owners make is focusing only on the headline rate. The true cost of borrowing may include origination fees, underwriting charges, renewal fees, collateral filing requirements, prepayment restrictions, and repayment timing.

Some products are presented with factor rates rather than APR, which can make comparison difficult if you are not looking closely. The safest approach is to evaluate the full repayment picture, not just the marketing language.

Repayment schedule matters just as much as pricing. A loan with daily or weekly debits can pressure cash flow, especially in industries with uneven collections or seasonal swings. Even when total cost is acceptable, the structure may still be wrong for your business rhythm. Strong financing decisions come from understanding both affordability and operational fit.

Documentation Checklist

Before applying, prepare the following:

- Business tax returns from the last two years

- Personal tax returns

- Profit and loss statements

- Balance sheets

- Recent business bank statements

- Ownership and formation documents

- Business plan or use-of-funds explanation

- Revenue projections

- Accounts receivable reports, if relevant

- Collateral documentation, if relevant

Having this material ready can reduce delays, strengthen lender confidence, and make it easier to compare offers across multiple funding sources.

What Lenders Look For in 2026

Most lenders are trying to answer the same question: can this business repay the loan reliably? To make that decision, they often review time in business, annual revenue, recent bank activity, credit profile, debt service coverage, industry risk, collateral, and overall financial organization.

Businesses with cleaner reporting and a more credible repayment story typically have more options and better negotiating power.

That means preparation is not just administrative. It is strategic. A borrower with organized tax returns, up-to-date profit and loss statements, balance sheets, bank statements, ownership documents, receivables reporting, and realistic projections usually moves through underwriting faster than a borrower scrambling to assemble documents at the last minute.

How to Improve Your Chances of Approval

Businesses can improve financing outcomes by keeping books current, separating business and personal expenses, maintaining healthy bank activity, reducing unnecessary debt burdens, and building lender relationships before capital becomes urgent. It also helps to present a clear use of funds.

Lenders respond better when the business owner can explain exactly why the money is needed, how it will be used, and how repayment will be supported.

In many cases, the most finance-ready businesses are not the ones with perfect numbers. They are the ones with organized records, realistic expectations, and a strategy that connects borrowing to measurable business goals.

Real World Scenarios

A restaurant in Chicago can use a line of credit to cover payroll in slow months while applying for an SBA 504 loan to purchase new kitchen equipment.

An ecommerce brand in Austin may use invoice financing to handle seasonal inventory surges while relying on revenue based financing to support ad campaigns.

A manufacturer in Ohio may secure an SBA 7a loan for expansion while using asset based lending for working capital.

Common Mistakes to Avoid

Many funding problems start after approval, not before it. Owners get into trouble when they stack multiple high-cost products, accept daily repayment pressure without testing cash flow, overlook guarantee language, or sign agreements without understanding the difference between factor rate and true borrowing cost. Another common mistake is borrowing reactively, after cash flow is already strained, instead of arranging financing while the business is still in a stronger position.

A better approach is to borrow with a clear purpose, compare multiple structures, and pressure-test repayment before signing. Financing should support the business, not dominate it.

Tips to Lower Loan Costs

Build a banking relationship early. Keep books clean and reconciled. Improve DSCR by reducing unnecessary expenses. Refinance high cost loans into lower rate products once eligible. Use loans strategically instead of reactively.

Final Thoughts

Business Loans in 2026 remain an essential tool for small and medium-sized businesses that want to stabilize operations, capture growth opportunities, and compete in a more demanding market. But not all funding is equal.

The best solution depends on your purpose, timing, financial profile, and tolerance for repayment pressure. SBA loans, bank loans, lines of credit, equipment financing, invoice financing, revenue based financing, and other products all serve different needs. Understanding those differences is what leads to smarter decisions.

Committed to Capital is positioned on the page as a partner that helps business owners compare options and pursue financing with greater clarity. When you prepare your documents, understand your numbers, and choose funding strategically, you put your business in a much stronger position to grow without taking on avoidable risk.