Securing loan approval with bad credit may feel like climbing a steep hill, but it’s far from impossible. Many small and medium-sized business owners face this exact challenge every day. A low credit score whether it stems from past financial mistakes, unexpected emergencies, medical bills, or simply a limited credit history does not lock you out of funding. What it does mean is that you’ll need a smarter, more strategic approach to get approved on terms that actually work for your business.

Key Takeaways

- Loan approval with bad credit is possible when lenders consider cash flow, collateral, and time in business, not just FICO scores.

- Secured loans, cosigners, and credit unions offer the highest approval odds for low-credit borrowers.

- Fixing credit report errors and reducing debt-to-income ratio can quickly improve approval chances before applying.

- Alternatives like PALs, BNPL, and crowdfunding can bridge funding gaps without traditional loan requirements.

- Preparation matters documentation, a growth plan, and a brief explanation of your credit history strengthen any application.

In this guide, we’ll walk through practical strategies, loan types, and alternative funding options so you can move forward confidently in 2026. Our goal is to help you not only understand how loan approval with bad credit actually works behind the scenes, but also position your business for long-term financial health.

Why Loan Approval With Bad Credit Is Still Possible

Banks and lenders look at far more than just a three-digit credit score. While a high score makes the process smoother, modern underwriters especially alternative lenders weigh several other factors that can tip the decision in your favor:

- Income stability – Is your business generating consistent monthly revenue? Lenders often want to see at least six months of steady deposits.

- Time in business – Many bad-credit lenders require a minimum of one to two years of operating history as proof of viability.

- Collateral – Do you have business equipment, inventory, real estate, or receivables that can secure the loan?

- Debt-to-income (DTI) ratio – How much existing debt are you already carrying relative to revenue? A DTI under 43% is generally viewed favorably.

- Cash flow trends – Lenders increasingly rely on bank statement analysis rather than FICO scores alone.

The reality is that loan approval with bad credit often comes with higher interest rates, shorter repayment terms, or stricter covenants. However, by demonstrating stability, responsibility, and preparedness, you can still secure the capital your business needs.

How to Improve Your Chances of Loan Approval With Bad Credit

Here are six proven strategies you can apply starting today.

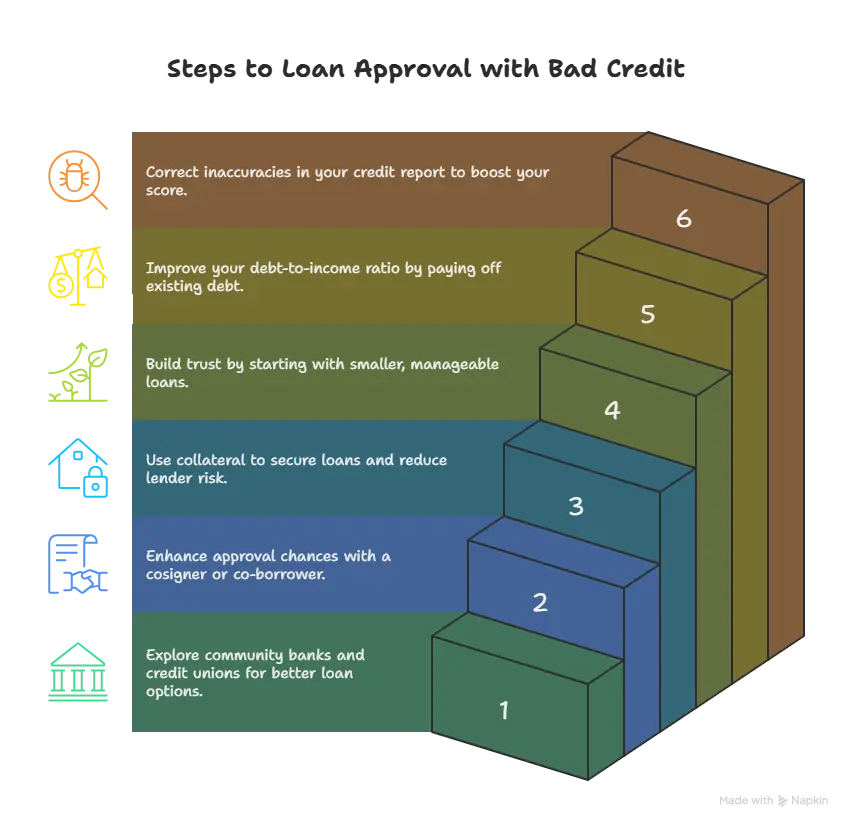

1. Find Lenders Who Specialize in Bad Credit

Not all lenders are the same. Community banks, online fintech lenders, and credit unions often provide more flexible options than traditional big banks. Credit unions in particular tend to have a community-first approach and lower credit thresholds, making loan approval with bad credit far more realistic. Online lenders like fintech platforms can also approve applicants in as little as 24 hours by using automated underwriting that weighs cash flow over credit score.

2. Apply With a Cosigner or Co-Borrower

If you can bring someone with strong credit to back your application, your odds improve dramatically. A cosigner shares legal responsibility for repayment, which reduces risk for the lender and can also lower your interest rate by several percentage points. Make sure both parties understand the obligation in writing that a missed payment affects both credit profiles.

3. Choose Secured Loans

Secured loans require you to pledge collateral such as business equipment, commercial real estate, accounts receivable, or savings accounts. Because the lender has a tangible asset to recover if you default, they’re far more likely to approve your request even with a credit score in the 500s. Common secured options include equipment financing, invoice factoring, and asset-based lines of credit.

4. FHA Loans

If you’re seeking a mortgage or commercial property loan, FHA-backed loans may work in your favor. With flexible requirements, they sometimes accept scores as low as 580 with a 3.5% down payment, or as low as 500 with 10% down.

5. Home Equity Loans or HELOCs

If you own property, tapping into your home equity is another way to get financing. This is a secured option, and lenders are often more willing to grant loan approval with bad credit when home equity is involved though you should weigh the risk of pledging your residence carefully.

6. Merchant Cash Advances

For businesses with steady credit card sales, a merchant cash advance provides upfront capital in exchange for a percentage of future sales. Approval rests almost entirely on revenue, not credit score though factor rates can be steep, so read terms carefully.

Alternatives to Loans for Bad Credit Borrowers

Sometimes the best option isn’t a traditional loan. Here are alternatives worth exploring:

- Secured Credit Cards – These help rebuild your score while providing small amounts of working capital. Most require a refundable deposit equal to your credit limit.

- Borrowing From Friends or Family – With clear written terms and a repayment schedule, this can be the most flexible and affordable option available.

- Payday Alternative Loans (PALs) – Offered by federal credit unions, PALs are capped at 28% APR far safer and cheaper than predatory payday loans.

- Buy Now, Pay Later (BNPL) – For smaller purchases, BNPL services let you split payments into installments without large upfront costs or hard credit checks.

- Cash Advance Apps – Useful for immediate, short-term needs, though they may charge small subscription or expedite fees.

- Crowdfunding – Platforms like Kickstarter, GoFundMe, or Kiva let you raise capital from supporters without affecting your credit at all.

Expert Tips to Strengthen Your Application

Before submitting any application, prepare like a lender will read it twice:

- Prepare Documentation – Two years of tax returns, six months of bank statements, recent invoices, and proof of revenue help show you’re financially organized and responsible.

- Write a Brief Explanation Letter – Many lenders will listen if you can explain why your credit dipped (medical event, divorce, business downturn) and what you’ve done since to recover.

- Highlight Your Business Growth Plan – Showing a realistic roadmap for revenue growth gives lenders confidence in your future ability to repay.

- Work With a Financial Advisor or Broker – Expert guidance can match you with lenders who specifically work with loan approval for bad credit applicants, saving you the credit-pull damage of multiple denied applications.

- Avoid Multiple Hard Inquiries – Each formal application can drop your score by 5–10 points. Apply only to lenders whose minimum requirements you actually meet.

Why Business Owners Choose Committed to Capital for Bad-Credit Financing

When traditional banks say no, Committed to Capital says let’s find a way. We’ve built our reputation on three core values: Commitment, Trust & Transparency, and Care and it shows in every funding decision we make.

From working capital and lines of credit to merchant cash advances and SBA-backed options, our financing solutions are designed for real businesses facing real credit challenges. No hidden fees. No confusing terms. Just honest funding from a team that treats your business like it’s our own.

Apply Online in Minutes and let’s get your business moving forward.

Final Thoughts

Getting loan approval with bad credit isn’t easy, but it’s far from impossible in 2026. By understanding your options, improving your financial profile, and targeting lenders who specialize in working with borrowers like you, you can secure the capital needed to move your business forward.

Every step you take reducing debt, fixing report errors, pledging collateral, or starting with a smaller loan moves you closer to approval and to better terms next time around. Remember: your credit score is just one part of your story. Show lenders you’re committed to repaying responsibly, and opportunities will open up.